The US dollar is down against the other major currencies during early Tuesday trading. We are in the runup to the release on Friday of July’s non-farm payrolls, which could, if figures fall significantly below the 900k consensus, vindicate the view of those Federal Reserve officials who believe it is too early to start tightening policies due to weaknesses in the labour market. Dollar bulls have been wrongfooted by this hesitancy amongst some prominent Fed figures, who believe that it is still too early to begin tapering asset purchases and Friday’s employment numbers could be a moment of clarity on whether or not those worries are justified and also mark a clearer pathway for the greenback.

Oil markets are holding losses following yesterday’s break-out of their short-term bullish channel. Market sentiment towards oil turned negative this week as more and more bearish drivers piled up, leading prices to a sharp but potentially limited correction. In fact, short-term investors scared by demand disruptions from China, caused by the rapid spread of the Delta variant in the region, are tempted to shift their exposure to more defensive sectors like cyclical values, financial and healthcare shares. Technically speaking, crude is now trading close to $71 following a bullish reaction over the 38.2% Fibonacci retracement level at $70.50. However, the rising bullish pressure displayed by the DMI indicator suggests the bearish correction may not be over yet. New supports can be found below $70 at first $69.45 and then $68.40.

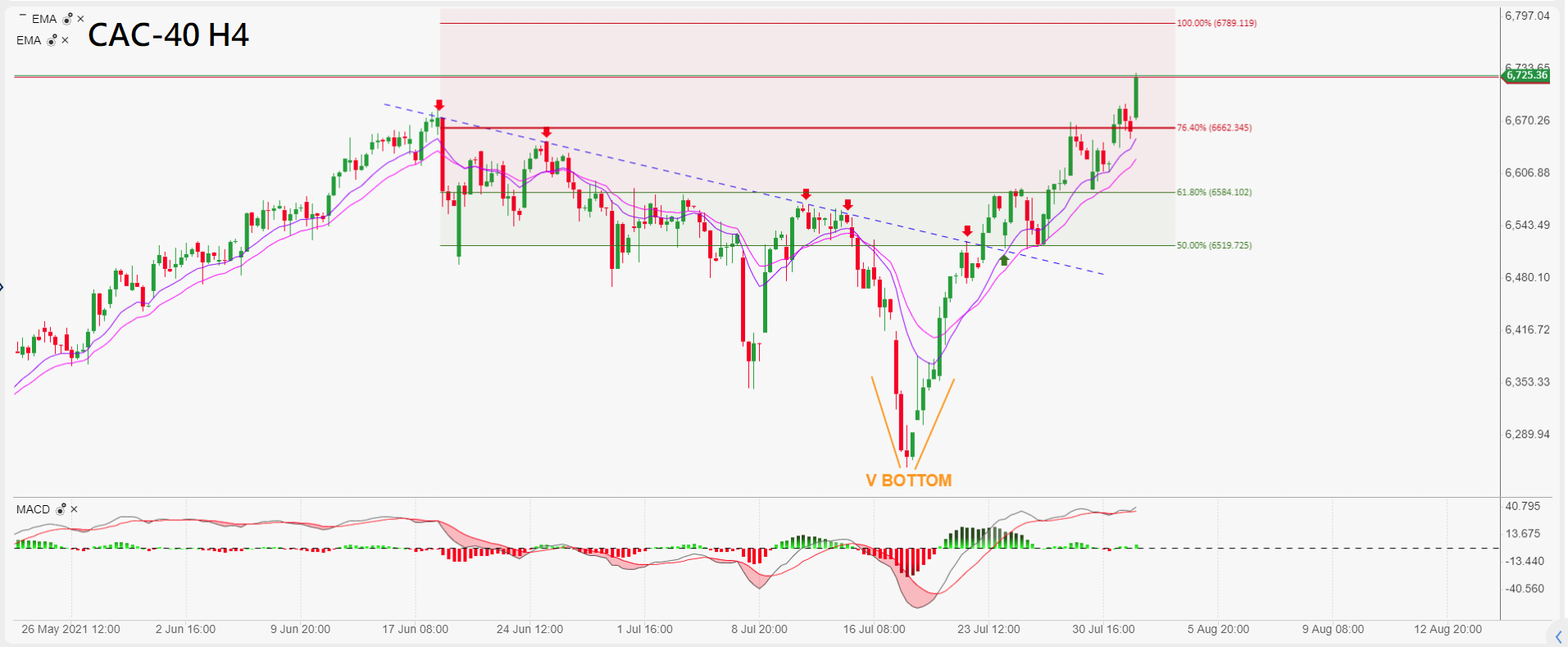

European share markets erased the gains registered shortly after Tuesday’s opening bell, following a mixed trading session overnight in Asia, as short-term uncertainty rises. China’s regulatory framework changes towards large private companies continue to scare stock investors all around the world as many still wonder which sectors are going to be targeted next. In addition, investors also have to deal with softer economic data than expected while the Delta variant continues to spread and threaten nations with further industrial impact. That said, no strong bearish price action is being registered so far and most benchmarks continue to trade sideways without clear direction, as investors remain in a “wait and see” trading stance ahead of key US data this week. The French CAC-40 Index is the eurozone’s best performer so far after prices successfully rebounded above 6,660pts, with the resistance at 6,790pts now in sight.

Pierre Veyret– Technical analyst, ActivTrades

Disclaimer: opinions are personal to the authors and do not reflect the opinions of LeapRate. This is not a trading advice.

Experienced writer and journalist, working in the global online trading sector, Steffy is the Editor of LeapRate. She has previous experience as a copywriter and has been with the company since January 2020. Steffy has a British and American Studies degree from St. Kliment Ochridski University in Sofia.