This article was submitted by Michael Stark, market analyst at Exness.

Most shares have traded more cautiously as the middle of the week approaches with key data on inflation from the USA. Oil has continued its recovery from last week’s fairly small consolidation while gold has moved up strongly since Friday’s NFP, not gapping down at Monday’s open. This midweek preview of data looks at USDMXN and GBPAUD.

There wasn’t a huge amount of action among central banks last week but markets were somewhat surprised by the Bank of England’s decision to leave its rate on hold. The FOMC’s meeting on Wednesday didn’t produce many surprises; however, participants now seem to be pricing in the possibility of not one but two rate hikes by the Fed before the end of the first half of next year.

This week doesn’t feature any meetings by major central banks, but the Banco de Mexico’s meeting tomorrow evening is a key event for the peso in the aftermath of Mexican inflation reaching a four-year high as announced yesterday. As in other countries, it appears to many traders that the BdeM needs to act in the face of sharply rising inflation.

Apart from this afternoon’s American annual inflation, crucial releases this week include Australian job data and British balance of trade and preliminary British GDP. The volume of British data tomorrow, as usual for second Thursdays, is likely to lead to significant intraday movement for the pound.

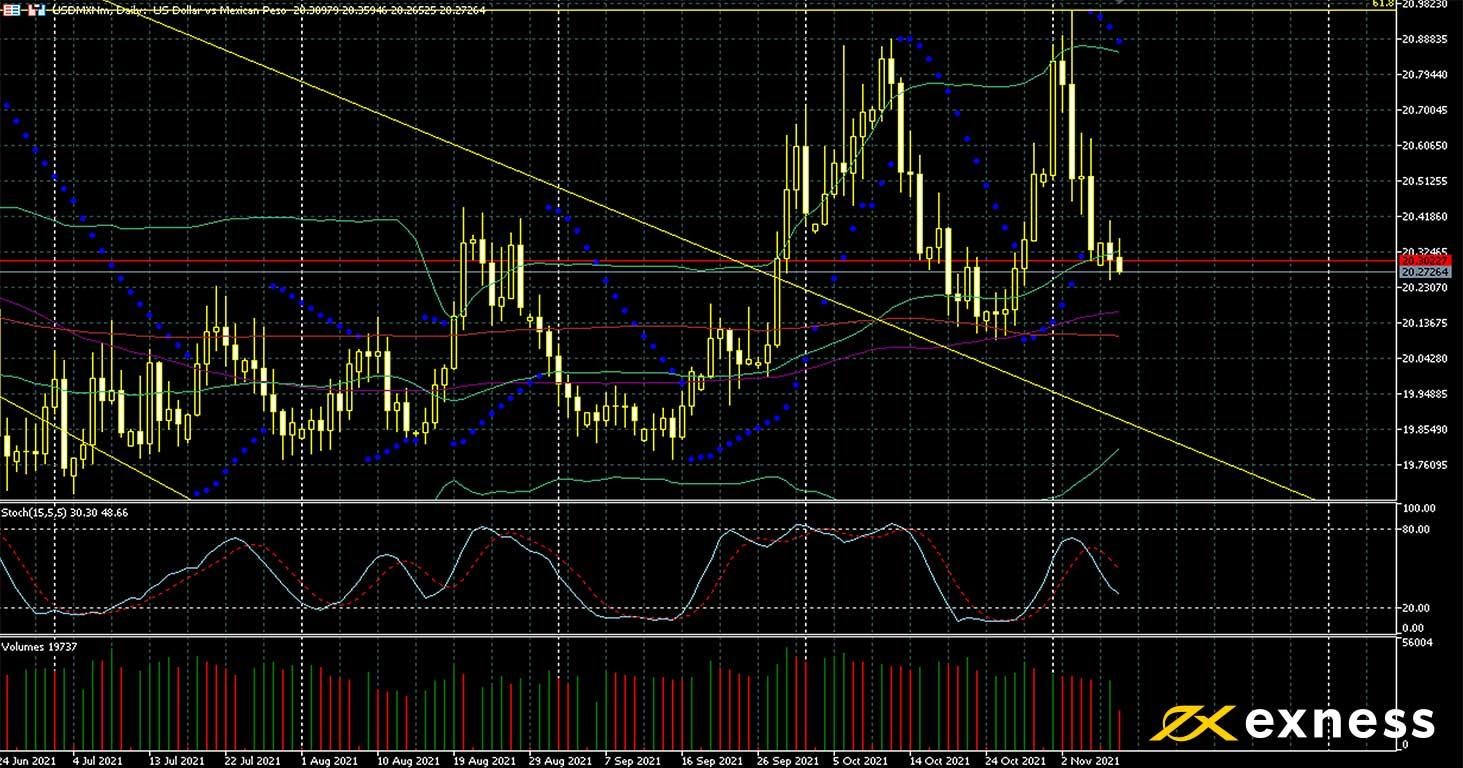

US dollar-peso, daily

Despite a slight uptick in the VIX this week, complacency in markets remains quite high and risk on is the general mo0d. This situation gives some support to exotics and trade-sensitive currencies against majors. The peso is also looking more positive to many participants because of high expectations that the BdeM will hike its benchmark rate again tomorrow in the late afternoon GMT: this would take the rate to a full 5%. Mexican annual inflation for October was 6.2%, more than double the target of 3%.

Looking at the chart, a breakout in either direction still doesn’t seem especially likely. The double top around Mex$20.85 last month and earlier this month would usually be seen as a sell signal, but the main support around Mex$19.70 is also strong given that it has remained unbroken since February 2020 despite repeated testing since this time last year. Waiting and gauging the response to tomorrow night’s news seems to be sensible in the context, especially considering likely high volatility this afternoon around American inflation.

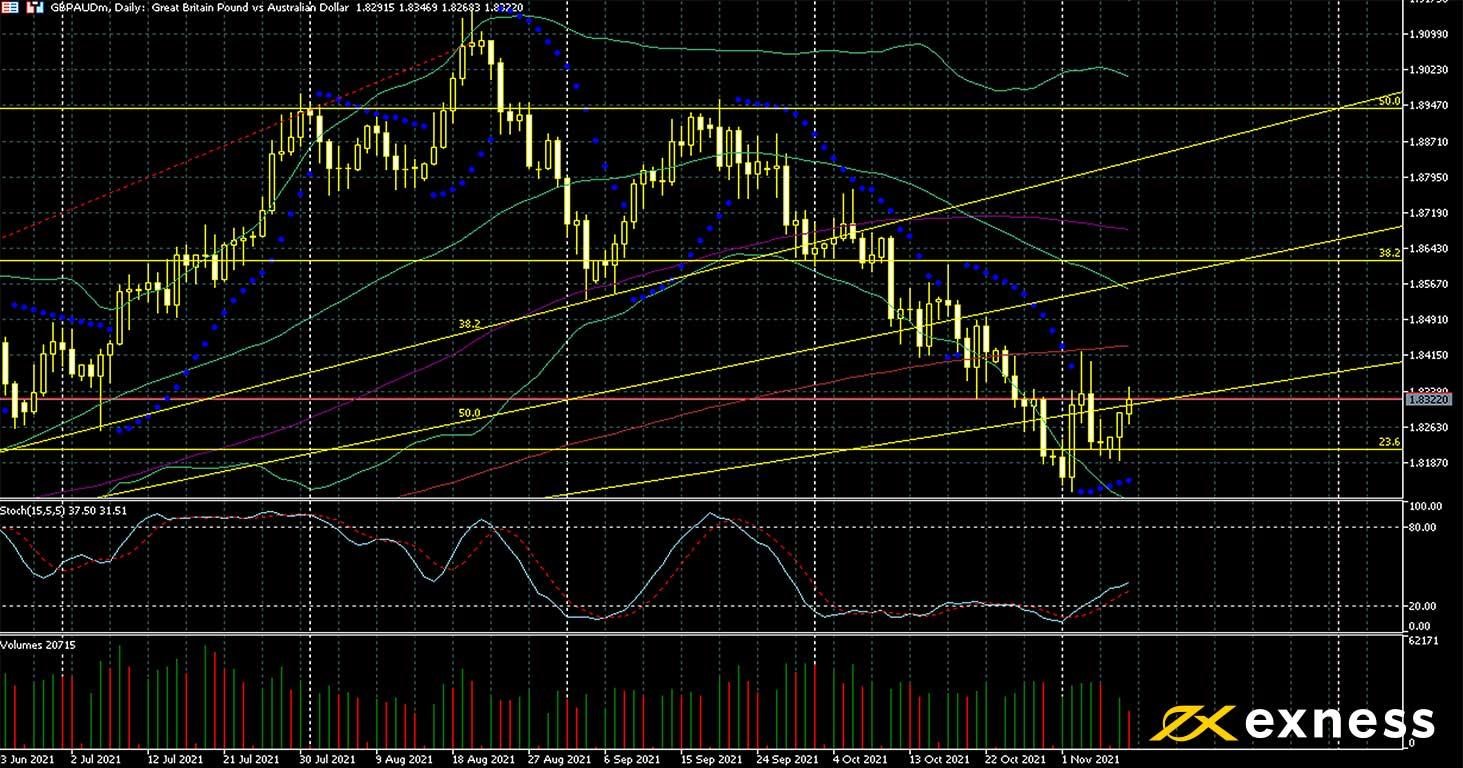

Pushback by the Reserve Bank of Australia last week against earlier rate hikes has dented sentiment on the Aussie dollar somewhat despite a generally friendly environment for trade-related and commodity currencies. The yields from Australian decade bonds have also corrected fairly sharply from above 2% since 1 November. For the pound, sentiment has recovered since last week as markets digested the likelihood of a rate hike by the BoE next month.

Considering TA, this does seem to be a likely place for a bounce. The initial rebound last Tuesday came in the area of the 23.6% weekly Fibonacci retracement and now seems to be on track to test the 200 SMA after recovering from a fairly large loss on Thursday. Since tomorrow is the second Thursday of the month and so a very big day for British data, volatility is likely to be quite high into the end of the week, with a move higher seemingly in view depending on the reaction to the key releases.

Key data this week

Bold indicates the most important releases for this symbol.

Experienced writer and journalist, working in the global online trading sector, Steffy is the Editor of LeapRate. She has previous experience as a copywriter and has been with the company since January 2020. Steffy has a British and American Studies degree from St. Kliment Ochridski University in Sofia.