As 2018 came to a close, several concerned observers of the crypto-verse predicted that 2019 would be a critical turning point for many crypto development efforts. In other words, it was time to demonstrate marketable “use cases” across the spectrum of over two thousand token programs that had raised significant funds based on rather thin whitepapers. Based on a new report from Hummingbot, an automated market maker provider, the first signs of a “culling process” may be underway.

As many analysts have been arguing for months, the “altcoin” moniker is far too inclusive, especially when one expects an “Alt-Season” to raise the “tides” for all development efforts, as if they belonged to one grouping. A new report now provides a delineating factor for sub-dividing altcoins into two distinct groups – the ones with liquidity and the ones without it.

According to the report provided exclusively to Crypto Briefing, researchers determined that:

The most liquid asset is 600x more liquid than the least liquid asset, and large-cap cryptocurrencies and stablecoins generally have the strongest liquidity.

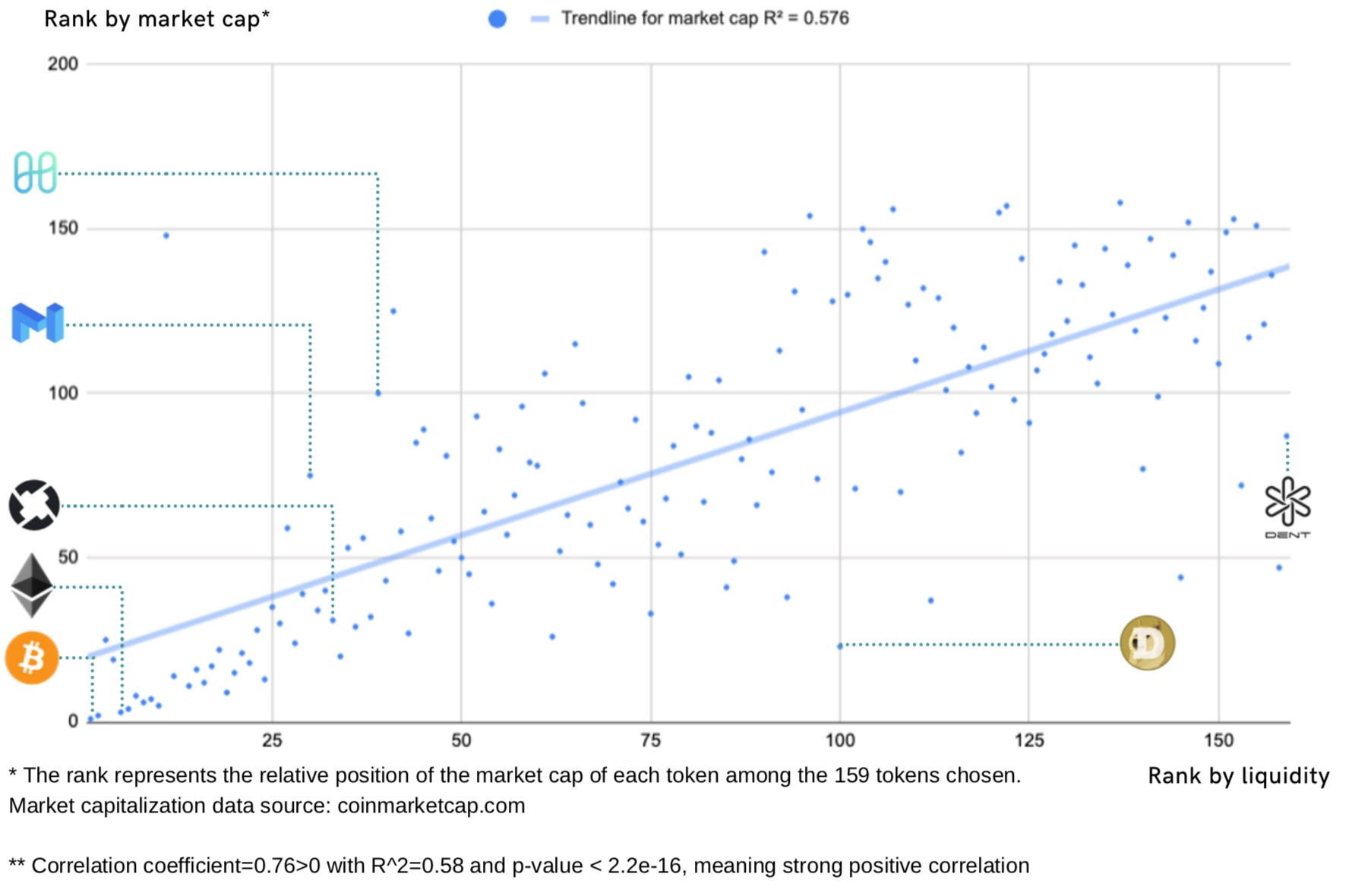

The report includes the following plot of rankings for 159 programs’ market cap versus liquidity:

In the past, analysts have attempted to correlate trading volumes with market cap data to arrive at a more appropriate rating scheme, but researchers at Hummingbot decided to focus on liquidity. Volume data in the industry has been found to be inflated for a variety of reasons and not a statistic that is creditable enough to yield valid insights. We reported back in September that Coinmarketcap.com announced that it “will be releasing new metrics based on liquidity to address the current concerns around inflated volumes”.

As Crypto Briefing reported:

The report uses slippage as a metric, which represents the difference between the price expected and price executed. Coins with high liquidity have lower slippage, as they have deeper order books so asks can be filled at different price points. Researchers at Hummingbot argue it’s a stronger metric than trading volumes, which can be easily manipulated by exchanges or the coin projects themselves.

As you might have speculated, Bitcoin was the program with the greatest liquidity, with Ether following close behind. Of the group presented, DENT, the token from Dent Wireless, proved to be the most illiquid by a multiple of “600X” the slippage of Bitcoin. The nearest challenger to DENT’s low level of liquidity was Pundi X (NPXS), a cryptocurrency and phone project. The two entities had respective market caps of $19 million and $48 million. The report also contended that:

Liquidity had consolidated further within a small group of assets and that there was a strong positive correlation between liquidity and market capitalization.

Hummingbot works in the liquidity field and perceives its role as to spread more liquidity across the entire crypto-verse. The problem, however, is that liquidity providers have to obey specific cost/benefit ratios in order to provide support for smaller programs. As the firm reports, professional market makers have shied away from smaller-cap tokens, since they have had “little incentive to perform the technical integration and maintain the requisite inventory for illiquid long-tail assets.”

The observed trend is that liquidity is concentrating in the top ten cryptocurrencies, and if this trend continues, other coin systems will become less viable, the early warning signs that a “culling process” is now currently taking place.