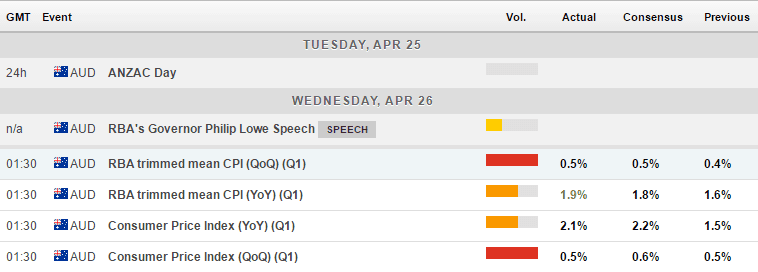

Trimmed mean inflation, the RBA’s preferred CPI measure sits just 0.1% beneath their 2% target to further remove any concerns over easing in the coming months, even if employment does turn lower.

Inflation data exceeded expectations today, which saw the trimmed mean CPI rise to 1.9%, up from 1.6% previously. This will be a delight to the RBA as this is close to their 2% target, yet they only expected a gradual rise towards this level over the medium term. Broad consumer prices expanded by 2.1% YoY, as the prior rise in oil prices made its way into the Q1 release. Yet QoQ% only managed 0.5% so we could see this plateau or fall further in the coming quarter/s.

The three main variables to monitor to assess the likelihood of chance to policy is from employment, inflation and household borrowing. Whereas weak employment or inflation could trigger a cut, high household borrowing is what could prevent them from cutting sooner. So as things stand there are no calls for a change of policy in either direction over the next 12 months, yet the potential for one could surface. Yet today’s inflation makes any calls for a cut even more remote.

Despite the positive dataset overall, AUD came under pressure and sold off against several currencies as traders booked profits. As there had been a consensus for inflation to move higher, traders had front run the release which saw those positions promptly closed when the data came out. However, we see the potential for AUD to regain traction against JPY and NZD although it remains under pressure from EUR and CHF following the French elections.

H1 closed with a bearish engulfing candle to warn of further weakness in the hours ahead, yet we also note it has remained above the daily pivot. Unless we see direct losses over the coming hours, then we could expect a jagged sideways correction before the rally resumes. We outlined our expectations for risk to remain supported overall in the coming weeks after the VIX 1-3 month spread provided a buy signals. As the moving averages remain in the correct bullish sequence and prices provide higher highs and lows, we expect a break to a new high in the coming week/s.

The gap higher following the French elections was not closed and, as it follows on from a major trough, we consider it a breakaway gap. This tends to appear at the beginning of a much larger move, so AUDJPY is one to consider in the weeks ahead if we do continue to see JPY outflows.

AUDNZD continues to regain traction after correcting from the 1.10 highs. We still think this can make its way towards 1.12-1.213 area over the coming weeks although we question if gains are likely to be as direct as the move from 2016 lows to 1.10. Note the bullish hammer which remain above the 1.0614 swing low to suggest the bullish move from the 2017 lows remain intact. However, as the pullback has been quite deep it does suggest AUDNZD next move higher (if it materialises) may not be as strong as the preceding move into the correction.

Currently resting around the monthly pivot, it has also stalled near a potentially bearish trendline. However, we think this will be broken to mark a bullish continuation in due course. The 1.10 area is an obvious level to consider profit taking initially yet, once the retracement from here is concluded we could then be headed for 1.12-1.13.