Market Overview

As Donald Trump approaches 100 days in office (will be on Saturday 29th April), markets have been preparing for his “huge” tax plan. However the announcement of Trump’s tax plan has left more questions than answers as the dollar and equities sell off. Markets have subsequently given the announcement a fairly luke-warm response. The main reason is that the plan does not appear to be budget neutral (i.e. it would raise the debt ceiling, something which fiscal conservatives in the Republican party are unsure of). A decision to cut corporation tax to 15% would be welcome if passed, but the tax rate of repatriation of overseas corporate earnings is vague. Subsequently the dollar has come under a little corrective pressure again, with Treasury yields pulling lower and equities coming off their recent highs. Is this a buy on rumour, sell on fact moment?

The Bank of Japan announced monetary policy overnight and decided to stand pat, however it did adjust its forecasts. Real growth for 2017/18 has been mildly revised higher to 1.6% (from 1.5%) as the central bank sees the economy “expanding” rather than previously just “recovering”, however this is tempered by a slight downward revision in inflation forecast to 1.4% (from 1.5%). The yen has mildly weakened on the back of this.

Wall Street closed lower on the day having been higher prior to the announcement of the tax plan. The S&P 500 was -0.1% at 2387, whilst Asian markets were also mixed to lower today with the Nikkei -0.2%. European markets have also opened lower, although the decline on the Eurozone markets could be tempered in front of the ECB. Forex markets show a general recovery against the dollar, although the euro is flat (again in front of the ECB) whilst the yen is mildly weaker after the BoJ cut its inflation forecasts. The Canadian loonie is an outperformer after the White House suggested that the NAFTA trade agreement (between US, Canada and Mexico) would be refined rather than scrapped. Gold is slightly back from yesterday’s late recovery, whilst oil is looking a touch corrective today.

The announcements of German inflation come throughout the morning but it is not until 1300BST when nationwide German CPI is announced and it is expected to pick back up to +1.9% on the year on year basis. However the markets will mostly be focused on the European Central Bank monetary policy with the rates announced at 1245BST. No change is expected to the main refinancing rate of 0.0% or the deposit rate of -0.4%, however the real interest will come in Mario Draghi’s press conference at 1330BST. With Eurozone data improving in recent months, market chatter is that the ECB could begin to discuss tapering asset purchases soon. With Eurozone inflation data to be announced on Friday this could be a little early this month but the ECB could drop its insistence that it stands ready to loosen monetary policy further if there is another downturn. US Durable Goods Orders are at 1330BST and are expected to grow by +0.4% on the month on an ex-transport basis. US Pending Home Sales are at 1500BST and are expected to be -0.6% on the month.

Chart of the Day – GBP/AUD

As sterling has sharply appreciated over the past couple of weeks, the Aussie has come under renewed downside pressure and this is having a significant upside drive on Sterling/Aussie. The market has rallied sharply to the extent that there was a move to a seven month high yesterday on an intraday push above the January high of 1.7205. On a near term basis there is also a bull flag on the close above 1.7110 which implies upside towards 1.7430. Momentum indicators are strongly positive with the RSI staying around the 70 mark, Stochastics remaining bullishly configured and the MACD lines rising strongly. Yesterday’s strong bull candle maintains the near term upside momentum with the hourly chart also strongly configured. The bulls will be looking for a close above 1.7205 which would then mean that the next resistance is not until the September high at 1.7800 which is the resistance of the ten month trading range. There is now support in the range 1.7110/1.7200 to buy into weakness, with the bulls remaining in control whilst above support at 1.6877.

EUR/USD

The market continues to hang on to the support of the longer term breakout above $1.0850. For the past two sessions this has been the basis of support for the low before the buying pressure has returned. This is an encouraging development for the bulls and suggests that corrections are still being seen as a chance to buy. The momentum indicators remain strongly configured even though the RSI has started to just lose its upside impetus. I continue to believe that a pullback into the $1.0800/$1.0850 range would be seen as a chance to buy as the longer term outlook has certainly improved with the continued position above the old long term downtrend. The hourly chart shows this to be more of a consolidation over the past few days under the resistance at $1.0950. That consolidation is not to be unexpected with the ECB meeting today. There is likely to be some volatility during the press conference.

GBP/USD

The consolidation on Cable is probably more interesting than it first seems. The dollar turned in a strong session yesterday across the forex majors, but made very little headway against sterling which remains supported above the $1.2775 breakout. The consolidation is more than a week old now and there is a positive bias that still flows through the technicals. A move above $1.2870 is now threatening today which would improve the near term outlook and re-open $1.2905 which was the spike high from last week. A closing breakout above $1.2905 would open the upside in a recovery once more. The psychological $1.3000 resistance would be first up, before $1.3060 and $1.3120. The hourly momentum indicators also suggest a positive bias with initial support at $1.2803 now above the $1.2775 basis of support.

USD/JPY

The recovery in the pair has come with yen weakness and a dollar bull recovery. However the longevity of this move is being questioned as the market has tested the overhead supply of 111.60 and started to struggle. Yesterday’s initially positive candle reversed to close down on the session as the rally failed at 111.77. This could be an early sign of the struggles of the rally at the confluence of the 111.60 pivot, the 38.2% Fibonacci retracement and the underside resistance of the old seven month uptrend. The early move today is mildly higher, but this means it will be very interesting to see how the bulls deal with the resistance once more. The hourly chart shows a less positive configuration on the hourly Stochastics and RSI. Another failure of a test of 111.60 would further question the rally. Support is now at 110.60. A close above 111.60 would be needed to open further recovery to 112.20.

Gold

The support of the old breakout at $1261 has been holding consistently over the past couple of days (aside from a brief dip to $1259.90 yesterday) and if this support continues to hold then the bulls will begin to build some confidence again. Give yesterday’s late rally to $1270.70, that makes today’s session very important. A close below $1261 would open for further correction back towards the next support around $1240. The concern is that daily momentum indicators remain corrective with the Stochastics and MACD lines falling away. However the old primary downtrend is a basis of support also around $1261 today. The hourly chart shows that a lot of work needs to be done to hold on to this support, whilst resistance is growing overhead below the $1278 key near term lower high.

WTI Oil

WTI posted gains in response to the mixed data in the EIA inventories, with the initial focus on the crude oil inventory drawdown which was -3.6m barrels and a bigger drawdown than the -1.7m barrels expected. However, the hourly chart shows that this rebound did not last too long before retracing back. The surprise build in distillates and gasoline stocks have questioned a recovery and pulled the reins on the bull move. This leaves WTI with a near term consolidation around the resistance band $49.60/$50.00. The bulls would be looking for a close above $49.60 for signs of a potential recovery, whilst the higher daily close above Tuesday’s high at $49.83 has already been encouraging for the bulls. Tuesday’s low at $48.87 is now posted as a near term support and the hourly chart shows how momentum indicators are beginning to turn a corner. Holding on to support at $48.87 will be key today. The buying pressure also needs to now breach the resistance at $50.20 as this is a growing near term pivot. Above $51.00 would begin to see the bulls developing traction in a recovery.

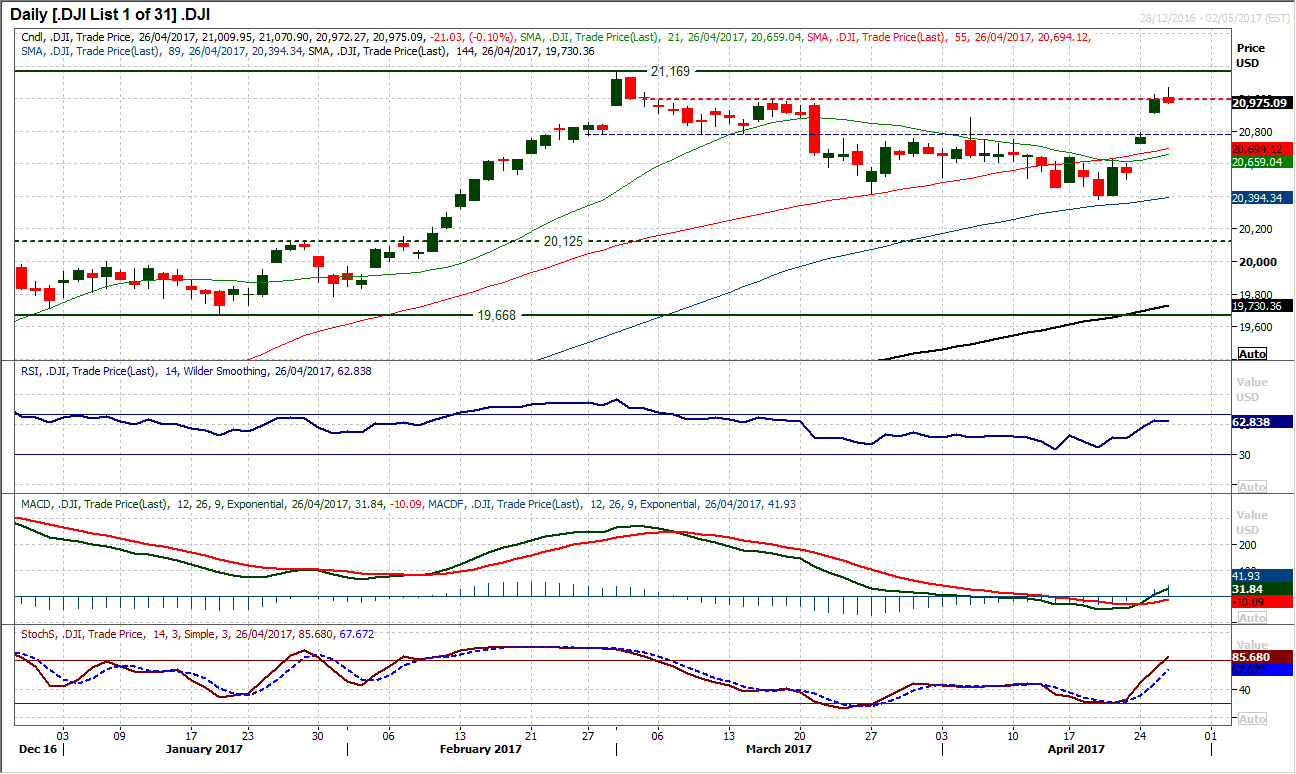

Dow Jones Industrial Average

The sharp Dow rally that has seen the market gap strongly higher on two days this week might just be beginning to stall. Yesterday’s session was cautious and only 100 ticks of range (the average true range is 160 ticks currently). Not only that, the market closed almost at the day low and yet again failed to close above the resistance at 21,000. The daily momentum indicators remain positively configured but looking on the hourly chart the position is not so clear for the bulls. A series of near term corrective signals have been posted across the hourly momentum indicators with MACD and Stochastics sell signals. The market closed lower on the day and now the bulls will need to hang on to the support band of Wednesday’s traded low at 20,909 and the previous breakout at 20,887. A higher low above this band of support would be bullish, but the corrective element of the chart is threatening near term now. Resistance at 21,070 now protects the all time high at 21,169.