The pound is trading lower against both the euro and the dollar during the early part of Tuesday’s session. Sterling has so far this year been one of the star performers amongst leading currencies. To a large extent pound gains have been supported by Britain’s successful vaccination program, which raised investors’ hopes that the complete reopening of the country on June 21 would generate a big increase in economic activity over the rest of the year. However, the recent upsurge in new virus cases, with numbers doubling every 10 days, is generating concerns that the UK’s ‘freedom day’ may have to be postponed, causing uncertainty in the markets and triggering pound weakness.

Stocks opened modestly higher in Europe on Tuesday, with gains in utilities offset by losses from automakers. No significant price action has been spotted so far and investors face much less volatile and directional markets this week due to the lack of market drivers. Most benchmarks are still flirting with historical highs and investors need more bullish catalysts to push stock prices further and justify an extended rally. Inflation remains in focus this week with traders likely to scrutinize each major data release, starting with today’s ZEW Economic Sentiment in Europe and the US JOLTs data for April.

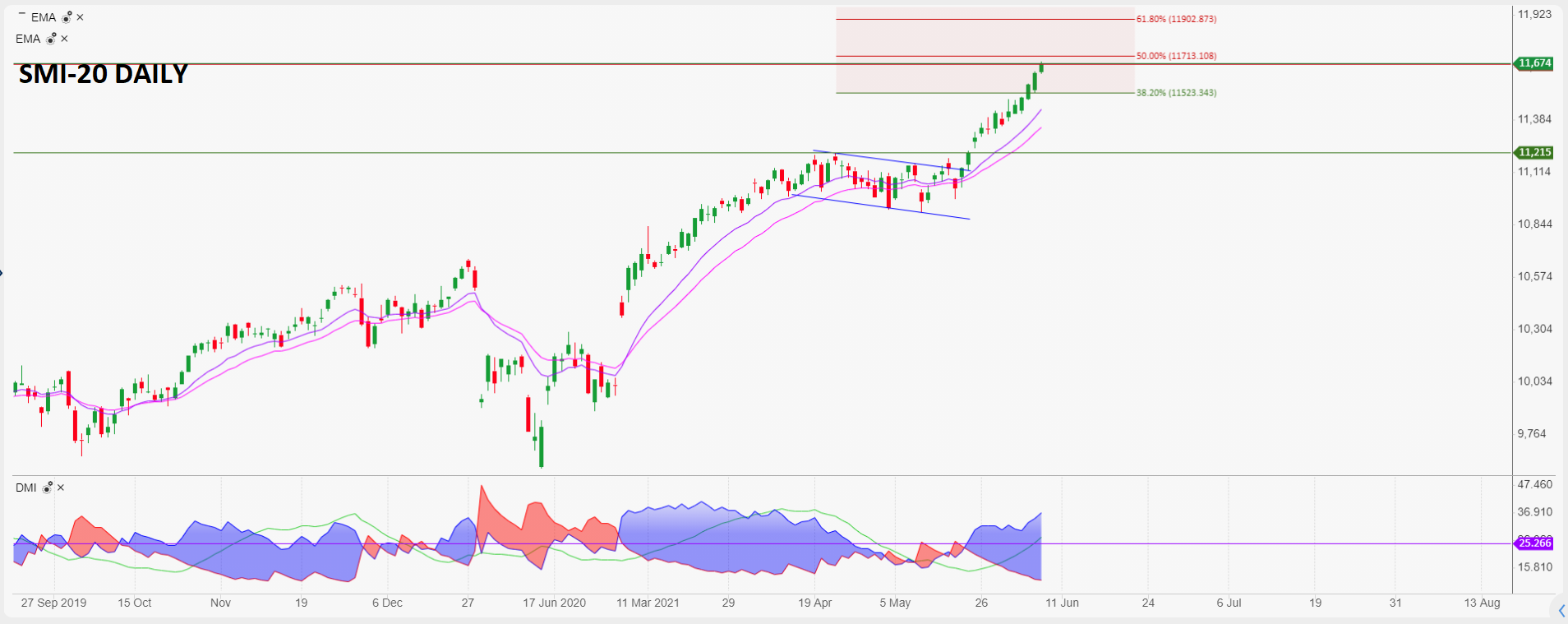

Technically speaking, most benchmarks are in green territory, with the SMI-20 Index from Zurich the best performer. The Swiss index is still trading well above 11,600pts, not too far from its next major resistance at 11,710pts, where a clearing could quickly lead the market towards 11,900pts amid an increasingly directional movement.

Experienced writer and journalist, working in the global online trading sector, Steffy is the Editor of LeapRate. She has previous experience as a copywriter and has been with the company since January 2020. Steffy has a British and American Studies degree from St. Kliment Ochridski University in Sofia.