Adam Vettese, UK Market Analyst at eToro, has provided his daily commentary on traditional and crypto markets for November 4, 2020.

Market futures in the US and further afield are choppy as the US Presidential election is currently still too close to call, with investors’ expectations of a ‘Blue Wave’ victory for the Democrats in the White House, Senate and House, looking increasingly unlikely.

US government bonds and stock futures all fluctuated wildly overnight as uncertainty over the election result mounted. Many states have declared, but some key battleground states are still too close to call, with absentee ballots taking much longer to count.

States including Pennsylvania, Michigan and Wisconsin – all key states taken from the Democrats by Trump in 2016 – are undecided so far but leaning Republican. The lack of clarity reflects a difficult moment for markets as uncertainty over who wins could extend for days, and perhaps weeks if results are disputed in the courts.

European markets have opened down as uncertainty prevails with the FTSE and Dax down 1 and 1.5% respectively. Expect trading to be particularly volatile today across the board and likely for the rest of the week.

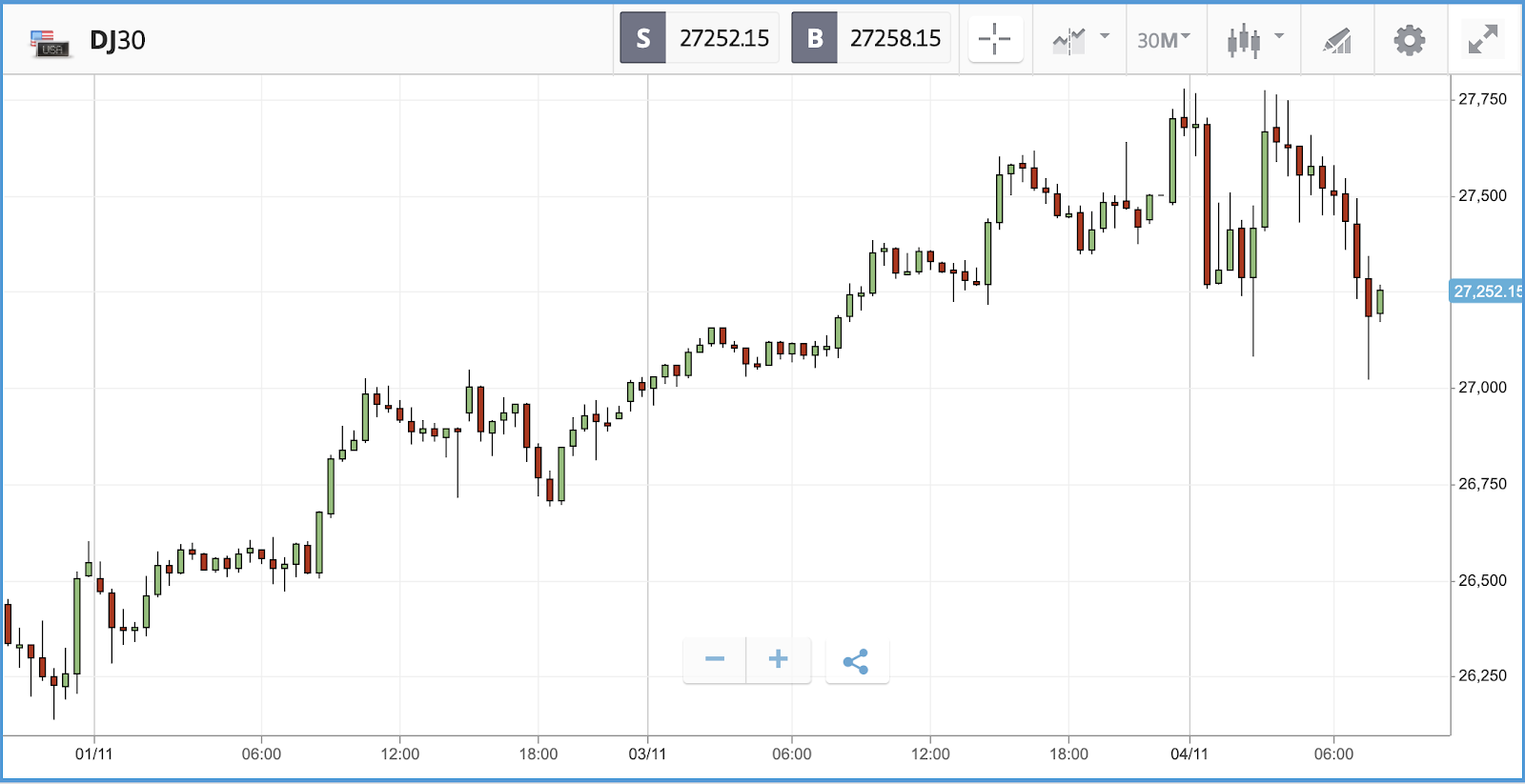

Stocks gained across the board on Tuesday ahead of election

On Tuesday all three of the major US stock indices made substantial gains, with the Dow Jones Industrial Average the biggest winner at +2.1% as investor optimism before election polls closed manifesting in buying activity across sectors. In total, 27 of the Dow’s 30 constituent stocks enjoyed a positive day, with none of the remaining three falling by more than 1%. Companies in a wide range of industries led the way, with Walgreens Boots, Goldman Sachs, Boeing and Walt Disney all up by more than 3%. Similarly, 10 of the S&P 500’s 11 sectors posted a positive day, with the industrials, financials and consumer discretionary sectors all gaining more than 2%.

Not all gains were election driven. Network equipment firm Arista Networks led the S&P 500 with a 15.4% gain after delivering expectation beating third-quarter revenue and profit figures. That is despite companies cutting back or delaying spending on network infrastructure due to the pandemic.

- S&P 500: +1.8% Tuesday, +4.3% YTD

- Dow Jones Industrial Average: +2.1% Tuesday, -3.7% YTD

- Nasdaq Composite: +1.9% Tuesday, +24.4% YTD

Crest Nicholson soars after increasing profit forecast, reinstating dividends

Similar to the US, London-listed shares were up across the board yesterday, with the FTSE 100 gaining 2.3% and the FTSE 250 up by 1.8%. Rolls-Royce, Natwest and Taylor Wimpey led the FTSE 100, with gains of 9.7%, 7.3% and 6.9% respectively. Banks were up across the board, with Barclays, Lloyds and HSBC all closing more than 4% higher. The FTSE 250 was led by housebuilder Crest Nicholson, which gained 16.5% after raising its profit forecast on the back of robust sales figures. The firm also announced it plans to reinstate its dividend. Broadly, homebuilders have been benefiting from demand that built up during the UK’s first lockdown, and homeowners looking for larger properties while stuck working from home.

- FTSE 100: +2.3% Tuesday, -23.3% YTD

- FTSE 250: +1.8% Tuesday, -20.1% YTD