Adam Vettese, UK Market Analyst at eToro, has provided his daily commentary on traditional and crypto markets for April 21, 2020.

US West Texas Intermediate (WTI) crude oil for May delivery traded as low as -$40 a barrel, the first time ever that sellers have paid buyers to take oil contracts off their hands. The price recovered to a positive $1.35 by evening in the US, but remains at historic lows due to the combination of crashing global demand and an inadequate production cut commitment from OPEC and its allies. US WTI crude has sunk well below other oil benchmarks as the main storage hub in Oklahoma, which is where contracts for the oil are delivered, is rapidly filling up. June contracts for WTI crude remain above $20 a barrel, while Brent crude June contracts are over $25.

One significant difference between the two types of oil is that WTI crude is typically moved by pipelines, whereas Brent is more often moved by sea, making WTI more difficult to move to locations where oil demand is higher. Today, the American Petroleum Institute will release data on US oil inventories (scheduled for around 2030 GMT), followed by the Energy Information Administration on Wednesday. Both sets of figures will be closely watched. The spot oil price is now trading just below the $21 level it has found support at over the course of the last five weeks.

Following the unprecedented negative oil prices, Asian shares posted their worst session in a month and European bourses have opened on the back foot with the commodities-heavy FTSE100 off by 1.5%, dragged down by oil giants BP and Shell — both down over 5.5% each.

Negative oil prices weren’t the only piece of breaking news on Monday. Late in the evening President Trump said that he intends to sign an executive order temporarily suspending immigration into the United States as the nation deals with the coronavirus pandemic. The White House provided no other details on Monday — immigration to the US is already heavily restricted, with refugee resettlement on hold and visa offices closed.

United Airlines also reported a $2.1bn loss for the first quarter of 2020, and revealed it has applied for $4.5bn in government loans in addition to $5bn in federal payroll grants and loans. The firm’s stock fell 4.4% following the news.

Energy names sink as US stocks start week on the back foot

Amid chaos in the oil markets, US stocks posted a negative start to the week, with the S&P 500 down 1.8%. The share prices of Chevron and ExxonMobil were down 4.1% and 4.7% respectively on the day, while troubled oil exploration firm Occidental Petroleum sank 7.6%.

In earnings news, tech firm IBM threw out its annual earnings guidance and announced sales for Q1 2020 were down 3.4% year-over-year due to the pandemic hitting software sales in March. The firm is on a lengthy mission to transform itself into a top tier cloud-first business services provider, and has struggled for years with falling revenues as it attempts to shake off its legacy IT business. IBM stock fell by more than 3% in after-hours trading after the results were revealed.

In the Dow Jones Industrial Average, which fell 2.4% yesterday, Boeing, Dow and Walt Disney were among the bottom five performers, along with Chevron and Exxon. Disney fell 4.1% as investors reacted to its decision to stop paying more than 100,000 workers during the shutdown while still planning to pay a $1.5bn dividend, while Boeing closed 6.7% lower after China Development Bank Financial Leasing canceled an order of 29 737 Max airliners.

Dow Jones Industrial Average: -2.4% Monday, -17.1% YTD

Nasdaq Composite: -1% Monday, -4.6% YTD

Airline stocks fall as bankruptcies start to hit sector

London-listed stocks were close to flat yesterday, with the FTSE 100 sinking to a substantial loss around lunchtime but recovering to a 0.5% gain by the close of play. On Monday it was announced that over 140,000 firms have applied to the government’s job retention scheme to help pay their wage bill, with Chancellor Rishi Sunak saying over a million people would benefit. Also on Monday, Bank of England deputy governor Ben Broadbent warned that economic recovery once the lockdown ends in the UK could be held back by consumer caution, pointing to subdued areas of consumption that remain in China.

The FTSE 100 was led by consumer goods giant Unilever, pest control firm Rentokil and industrial equipment rental company Ashtead Group, which posted gains of 4.6%, 4.5% and 4.1% respectively. At the tail end of the FTSE were some of the UK’s largest homebuilders, along with airline names. It was a dismal day of headlines for airlines, with four subsidiaries of Norwegian Air filing for bankruptcy, and Virgin Atlantic announcing that it will only survive the pandemic with a government bailout – while Virgin Australia also entered administration. British Airways parent International Consolidated Airlines Group (IAG) and easyJet closed Monday 3.3% and 4.2% lower respectively.

FTSE 100: +0.5% Monday, -22.9% YTD

FTSE 250: -0.2% Monday, -27.7% YTD

What to watch

Netflix: Some of America’s largest companies report earnings today, but Netflix will be among the most interesting to watch. The firm is arguably one of the biggest potential beneficiaries of people being stuck at home, but also faces the challenge of how to produce fresh content with social distancing requirements in place. Analysts will be watching the company’s post-market close earnings on Tuesday closely, specifically looking for data on subscriber numbers, and whether management anticipates that any recent step up in users will be permanent, or whether they are anticipating a drop-off once things return to normality. Analyst expectations for the firm’s Q1 performance have jumped from an earnings per share figure of $1.20 three months ago, to $1.64 now.

Coca Cola: Drink and snack giant Coca-Cola reports its Q1 2020 results first thing today; investors will get a look at how the shutdown of restaurants, travel and entertainment events have impacted the company’s sales. Coca-Cola stock fell by as much as 40% in the broader market sell-off, but has gained 23.9% over the past month and is now only down 15.9% year-to-date. Analysts will also be probing the firm for how China’s lockdowns impacted its sales, as the Chinese market is one of its largest. One potential positive outcome of the global lockdowns for the firm is consumer stockpiling, which may have provided some respite. Currently, 13 Wall Street analysts rate the stock a buy, three an overweight, and five a hold.

A selection of other significant US names reporting today: Lockheed Martin, Texas Instruments, Chipotle, Snap, Philip Morris, Northern Trust.

Claimant count change: Today UK unemployment claimant count figures for March will be released, which will provide insight into how the labour market has been hit by the pandemic. The figure is the equivalent of the US’s initial jobless claim numbers, which have shown more than 20 million people in the US have signed on for unemployment benefits over the last four weeks. Predictions for the number of new claimants in the UK for March are some 10 times higher than the February number, with a figure of close to 200,000 anticipated.

Crypto corner

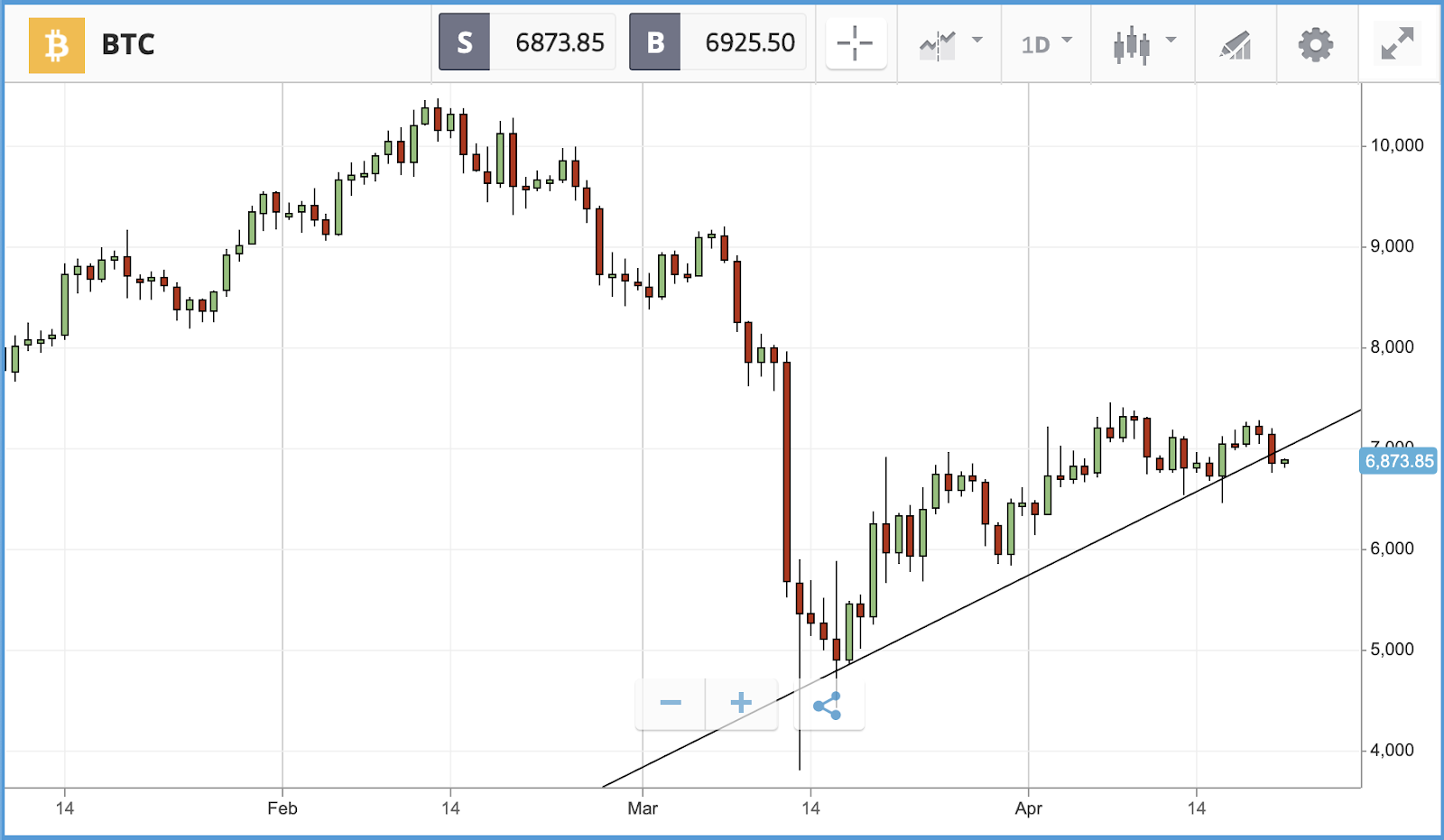

Bitcoin’s month-long uptrend is noticeably running out of steam as the price consolidates ahead of the halving on 12th May. The price has been suppressed back below the psychologically important $7,000 level as miners who are soon to be unprofitable exit the space — until now, this had been outweighed by bulls pushing the price up from its mid-March trough. That said, bitcoin barely flinched as negative oil prices sent shockwaves through traditional markets and in relative terms has held up very well.

Elsewhere, the US Commodity Futures Trading Commission (CFTC) has approved Bitnomial as a venue to offer bitcoin futures and options. The main difference being that these derivatives will be settled with physical bitcoin, as opposed to the fiat equivalent that CME Group offers for example.

All data, figures & charts are valid as of 21/04/2020. All trading carries risk. Only risk capital you can afford to lose.

This is a marketing communication and should not be taken as investment advice, personal recommendation, or an offer of, or solicitation to buy or sell, any financial instruments. This material has been prepared without having regard to any particular investment objectives or financial situation, and has not been prepared in accordance with the legal and regulatory requirements to promote independent research. Any references to past performance of a financial instrument, index or a packaged investment product are not, and should not be taken as, a reliable indicator of future results. eToro makes no representation and assumes no liability as to the accuracy or completeness of the content of this publication, which has been prepared utilizing publicly-available information.