This article was submitted by Michael Stark, market analyst at Exness.

American and European shares generally bounced yesterday as dip buyers emerged from the recent decline in prices. The central focus of data this week is on American annual inflation this afternoon at 12:30 GMT, which is likely to have a strong effect on the dollar. This midweek preview of data looks at USDJPY and EURGBP.

The Fed raised its funds rate by half a percent last week as was almost universally expected, giving further support to the dollar in most of its pairs. However, the Bank of England’s meeting on Thursday surprised markets by resulting in a hike of only 0.25% against the expectation for a two-step hike. Sentiment on the pound took another hit as the possibility of recession in the UK was raised. This week traders are looking ahead to the Banco de Mexico’s meeting on Thursday night, with the consensus pointing to a half percent hike to 7%.

Apart from the critical American CPI this afternoon, other key data this week include British preliminary GDP on Thursday morning and Michigan consumer sentiment on Friday. With high activity and relatively high volatility in stock markets and amid cryptocurrencies’ sharp decline on Monday, this is likely to be an active few days in markets, especially for forex, metals and shares this afternoon.

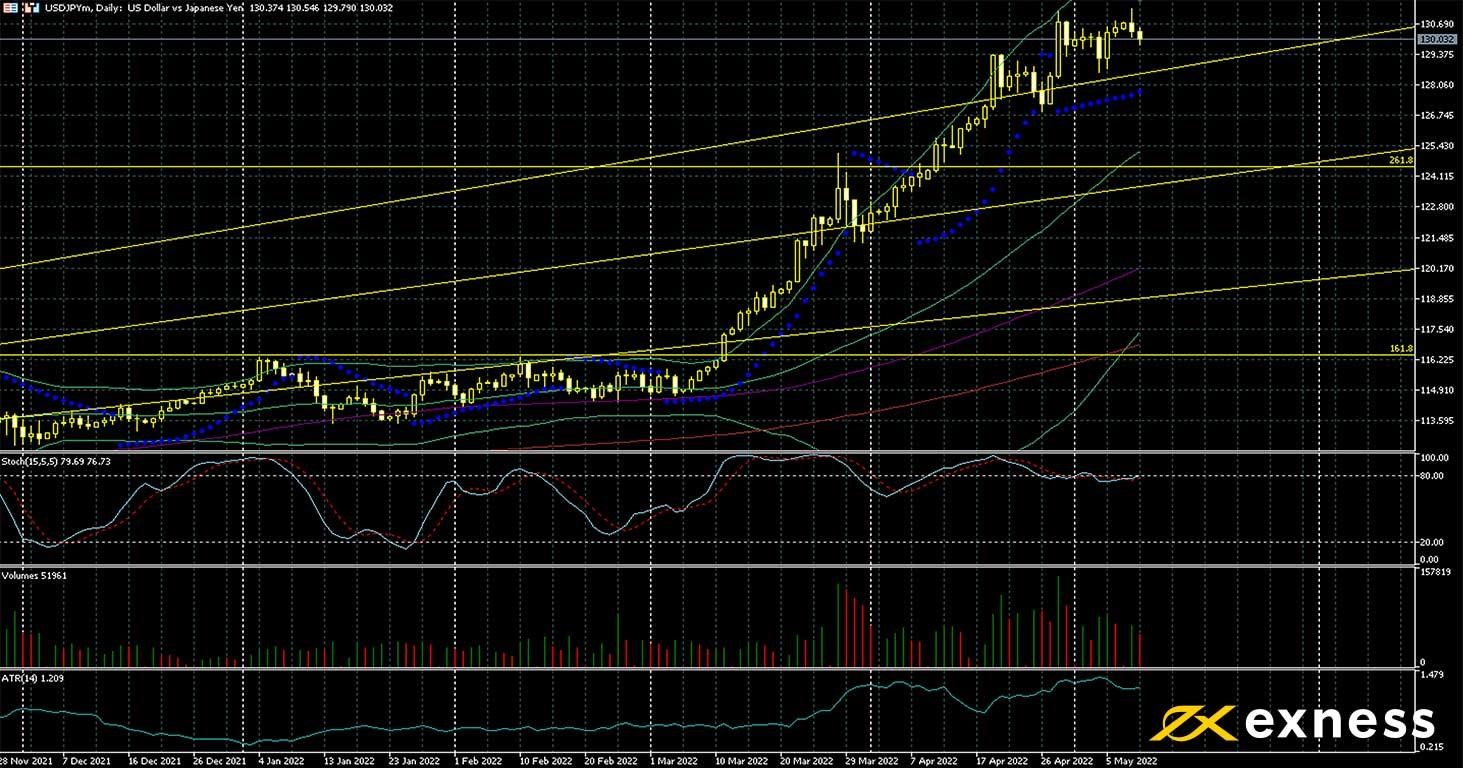

Dollar-yen, daily

The yen has remained weak in May so far as the increasing divergence in monetary policy is clear. Some reports on Monday suggested that the USA and Japan are considering a coordinated intervention to reduce the rate of dollar-yen, but markets seem to have discounted these rumours so far. Meanwhile the dollar index touched 104 yesterday, a fresh 20-year high, as CME FedWatch Tool projects a 100% probability of at least a two-step hike by the Fed at its next meeting. Yields of decade Treasuries retreated yesterday but remain only slightly below 3%.

Given the psychological importance of ¥130, lower buying volume so far this month and overbought based on the slow stochastic, technical analysis would suggest that further strong gains in the near future are unfavourable. However, higher than expected inflation this afternoon could drive the dollar strongly in the short term at least. The long-term target to the upside based on Fibonacci would be the 423.6% weekly extension around ¥138. Before that might be reached, though, a retracement back to the area of ¥127 would be more likely and provide a less risky entry for buyers.

While the euro is still at a six-year low against the US dollar, the situation against the pound sterling has been quite different in the aftermath of last week’s very negative meeting of the Bank of England. The risk of stagflation remains high in the eurozone and the ECB is almost certain to be much slower than the Fed and BoE in raising rates. However, the BoE announced last week its expectations that the British economy will stagnate this quarter before contracting around 1% in Q4 2022. For now, the war in Ukraine isn’t particularly in focus for traders, so this factor’s removal has helped the euro somewhat.

Similarly to dollar-yen above, overbought conditions after a very strong upward movement would suggest consolidation before any attempt to push higher. However, ATR at around half a penny is at its highest in nearly a year, which might suggest a relatively short pause before possible resumption of gains. The 61.8% weekly Fibonacci retracement around 86.4p seems to be the next strong resistance, while 31 March’s intraday at 85p could be the main near-term support.

Thursday is an extremely active day for British data, with preliminary GDP for Q1, balance of trade and various industrial releases all due at 6:00 GMT. The pound’s reaction to these figures could be quite dramatic, so it would traditionally make sense to wait until the dust settles or at least keep positions small if they’re to be held throughout the day tomorrow.

Key data this week

Bold indicates the most important releases for this symbol.

Experienced writer and journalist, working in the global online trading sector, Steffy is the Editor of LeapRate. She has previous experience as a copywriter and has been with the company since January 2020. Steffy has a British and American Studies degree from St. Kliment Ochridski University in Sofia.