This article was submitted by Michael Stark, market analyst at Exness.

European shares bounced slightly in general early on Monday with many Asian markets closed for lunar new year. Markets are continuing to digest the apparent shift in sentiment on American monetary policy, with gold looking weak in early trading on 31 January. This preview of weekly data looks at AUDUSD and EURGBP ahead of the Bank of England’s meeting, the NFP and key releases from Australia over the next few days.

There wasn’t much definite activity by central banks last week except for the South African Reserve Bank’s hike of its repurchase rate to 4%. However, markets increasingly expect more hawkishness from the Federal Open Market Committee this year. The likelihood of a hike to at least 0.25-0.5% on 16 March is 100% according to CME’s FedWatch, and the majority expects a target range of 1.25-1.5% by the end of the year.

This development in sentiment has been strongly negative for gold while propelling the dollar up. Elsewhere, the Bank of England is meeting on Thursday, with a hike to 0.5% expected, while the Reserve Bank of Australia early on Tuesday is likely to announce the end of its quantitative easing. The European Central Bank’s meeting on Thursday is unlikely to have much effect on markets.

Friday’s NFP dominates regular data this week, with focus also on average hourly earnings and the rate of unemployment in the USA. European job data and inflation are expected on Tuesday and Wednesday, and Australian balance of trade on Thursday morning rounds off the important figures.

This is quite an active few days of earnings. Activision, AMD, Alphabet, Amazon and ExxonMobil are among the big names releasing earnings reports on Tuesday and Thursday, so activity in American stock markets might increase around the middle of the week.

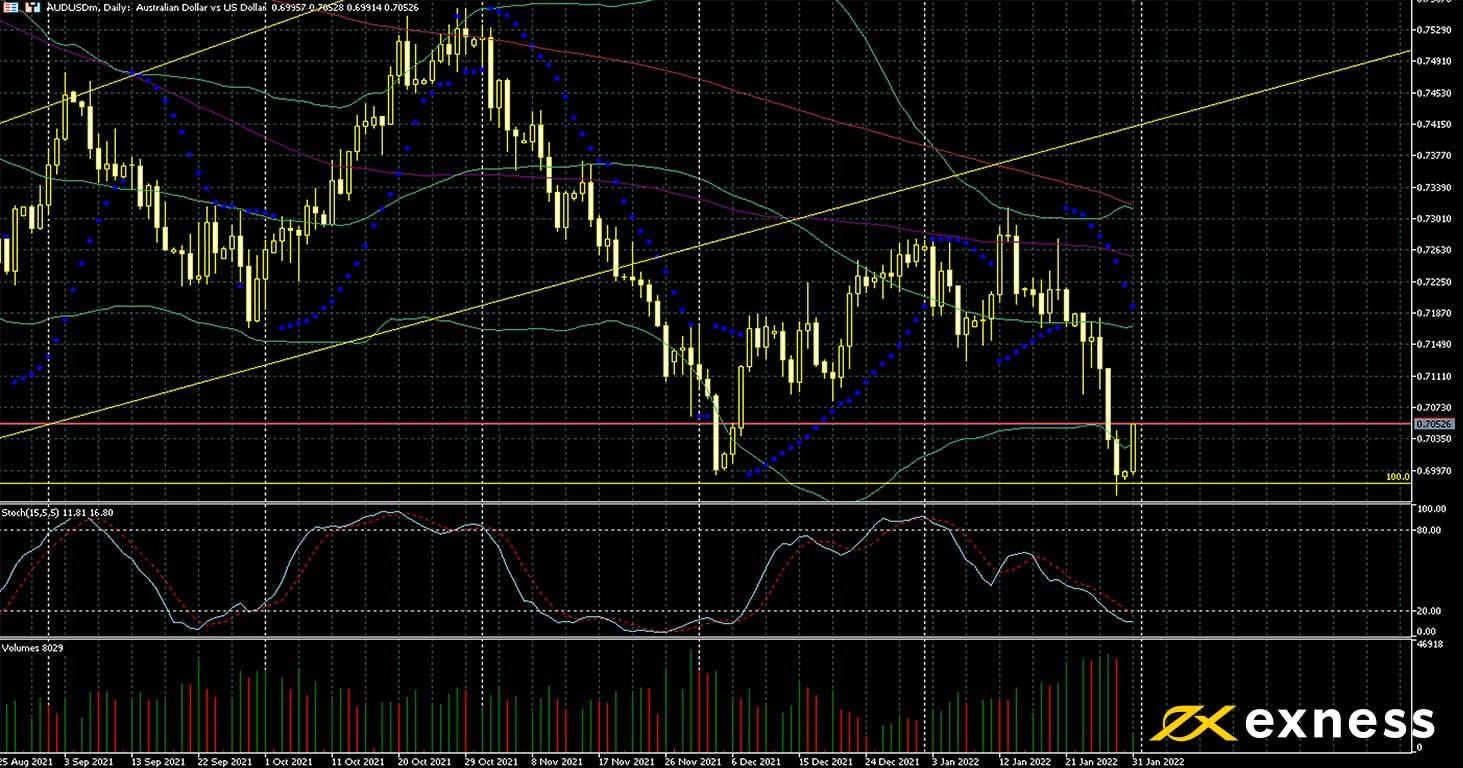

Australian dollar-US dollar, daily

The Aussie dollar bounced against the greenback on Monday in what seems to be a technical movement around the 100% Fibonacci retracement. The Fed’s increasing hawkishness combined with uncertainty on the schedule for the RBA’s tightening has given the US dollar a boost here, while general risk-off sentiment is bad for trade-sensitive currencies like AUD. However, ongoing recovery in the prices of industrial commodities – most notably iron ore – might generate tailwinds for the Aussie dollar given Australia’s reliance on exports of these.

The 100% weekly Fibonacci retracement, i.e. full retracement of losses in Q1 2020, is the main technical reference here and still a very strong support. A clear break below this would probably need a new catalyst from the RBA on Tuesday or Thursday morning’s balance of trade. Usually, a single NFP is unlikely to have a sustained effect on markets, but activity is likely to be high on Friday afternoon GMT. To the upside on the chart, the 50 SMA from Bands around 71.7c seems to be the first clear resistance.

Sentiment on the pound has been somewhat weaker since last week as the British government faces intense criticism over its ‘lockdown parties’ in 2020, with the imminent full report expected to damage Boris Johnson’s leadership further. However, the Bank of England is widely expected to hike its rate on Thursday, which would take it to 0.5%.

As above for AUDUSD, the 100% weekly Fibonacci retracement area is the main support which price is currently testing. A breakout below here might (eventually) open up prices below 80p for the first time since 2016’s referendum on Brexit. However, traders should monitor oversold with the slow stochastic currently around 19 and possibly consider waiting for at least a small bounce before selling in.

EURGBP is likely to be quite volatile on Thursday from noon as decisions from the BoE and ECB are expected within an hour of each other. Tuesday is also a fairly important day of data from the UK and eurozone.

Key data this week

Bold indicates the most important releases for this symbol.

Experienced writer and journalist, working in the global online trading sector, Steffy is the Editor of LeapRate. She has previous experience as a copywriter and has been with the company since January 2020. Steffy has a British and American Studies degree from St. Kliment Ochridski University in Sofia.