This article was submitted by Michael Stark, market analyst at Exness.

European stock markets started the week generally higher amid strong earnings in most sectors and American light oil has reached a fresh seven-year high this morning. Participants in markets continue to focus this week on inflation and its effects on commodity markets. Today’s preview of weekly data looks at UKOIL and EURAUD ahead of key regular data and the European Central Bank’s meeting on Thursday afternoon GMT.

There were two major surprises from central banks last week. Firstly, the Central Bank of the Republic of Turkey cut its one-week repo rate to 16%, a slash of a full two percent. This combined with recent diplomatic issues between Turkey and various EU nations is likely to lead to continuing losses for the lira (symbol TRY) this week as investors’ confidence in Turkey remains extremely low. The Central Bank of the Russian Federation also surprised markets by raising its key rate to 7.5%, a quarter of a percent more than expected.

This week’s highlights in monetary policy are the ECB’s meeting on Thursday and the Bank of Canada’s on Wednesday at 14.00 GMT plus, to a lesser extent, the Bank of Japan early on Thursday morning. No significant change to policy is expected, but how senior policymakers comment on economic conditions and especially inflation is likely to drive movement in markets and further speculation on the timeline of tapering QE.

In the context, this week’s biggest regular data are inflation from Australia, Germany, the eurozone and France plus American annual GDP (advance) on Thursday afternoon. Earnings season continues in the USA, with this week being the biggest in terms of large tech companies, so stock markets’ reactions might have strong knock-on effects for forex and some commodities.

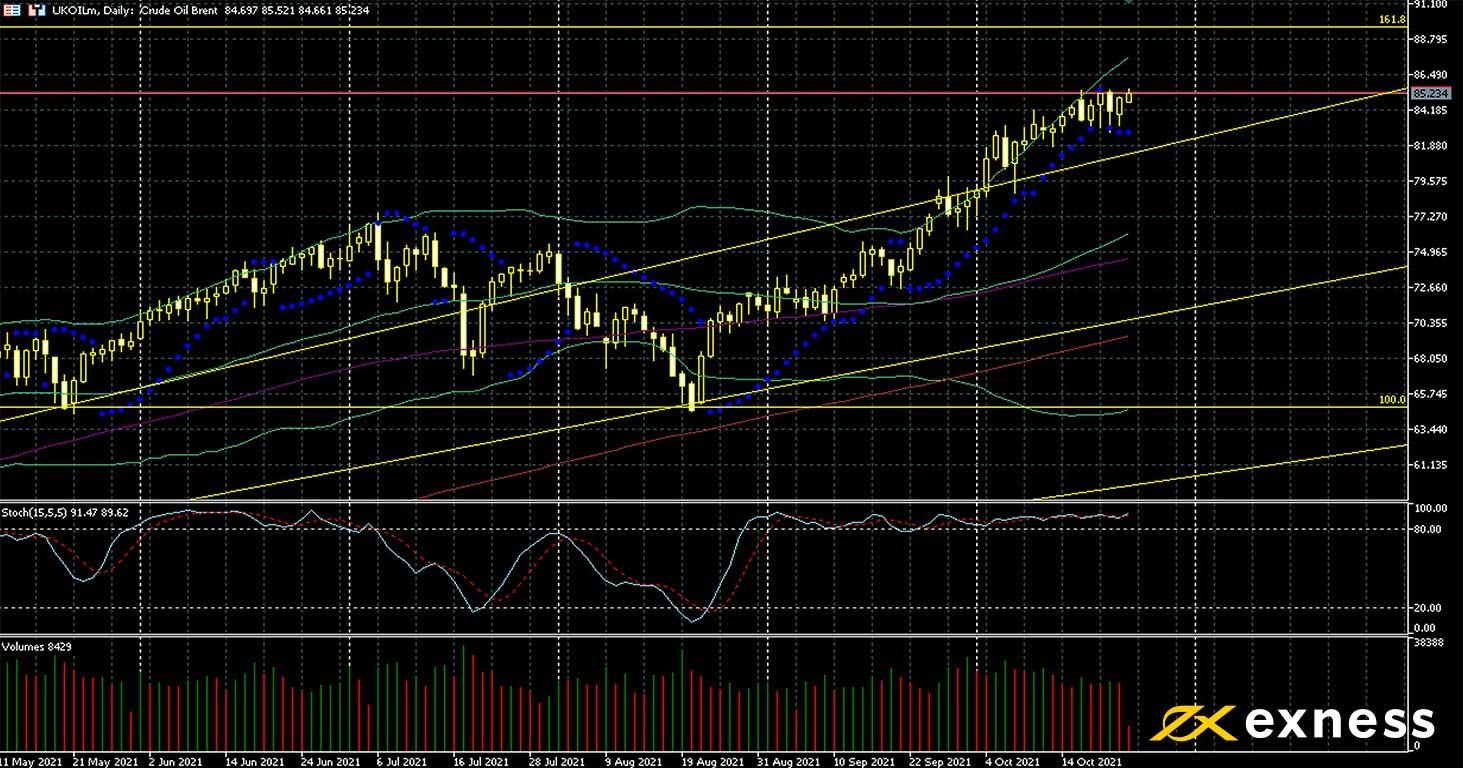

Brent, daily

Brent’s intraday high on Monday of $85.52 is the highest price since October 2018. Demand has remained strong over the last few weeks and supply tight. Saudi Arabia, Nigeria and other key members of OPEC seem to favour caution still when it comes to possible further boosts to supply over the next few months. Friday night’s Baker Hughes rig count also printed the first drop in active American rigs for nearly two months.

The clear target for old buyers is the 161.8% weekly Fibonacci extension just below $90. Finding an entry as a new buyer is likely to be difficult here, but a bounce seems possible from the 38.2% zone of the weekly Fibo fan and definitely from the psychological area around $80. Brent has been strongly overbought based on the slow stochastic since August: this doesn’t necessarily mean ‘wait until there’s no buying saturation’ but that new buyers should pay particular attention to appropriate entries. This week’s regular data, primarily the EIA’s stocks, could provide some if intraday volatility increases.

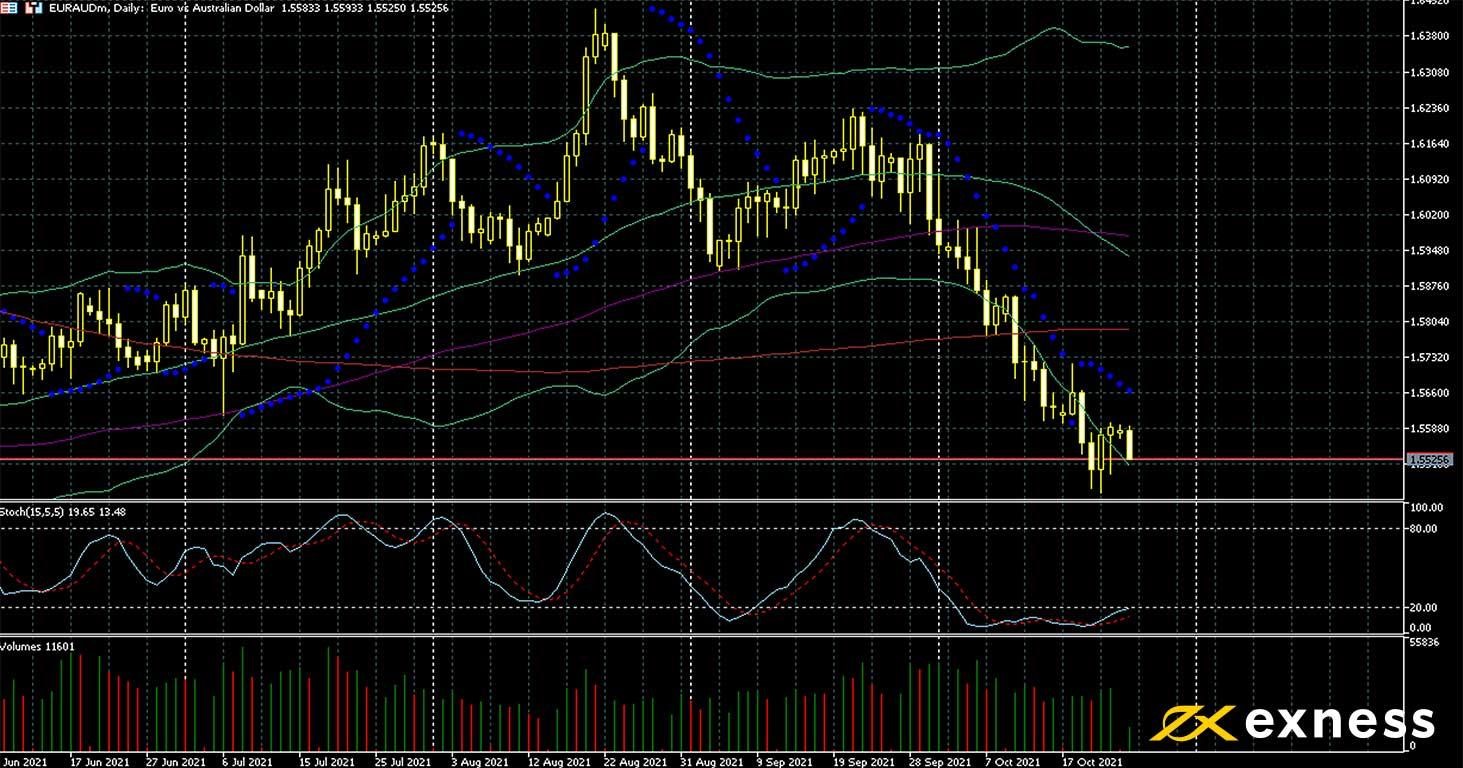

Strong gains by many industrial commodities since summer and perceptions that the ECB is slow in winding back QE have combined to drive the ongoing round of losses for the euro against the Aussie dollar this month. The RBA is now among the more hawkish central banks and might raise its cash rate sooner rather than later next year.

A retest of the lows from February and March this year below $1.53 doesn’t seem favourable immediately. However, more losses towards the next possibly important psychological area around $1.54 are in view unless the ECB’s tone switches toward the hawkish on Thursday. New sellers would probably look for another failed test of $1.56 before entering. This might come during or around Australian inflation early on Wednesday morning GMT.

Key data this week

Bold indicates the most important releases for this symbol.

Experienced writer and journalist, working in the global online trading sector, Steffy is the Editor of LeapRate. She has previous experience as a copywriter and has been with the company since January 2020. Steffy has a British and American Studies degree from St. Kliment Ochridski University in Sofia.