This article was submitted by Michael Stark, market analyst at Exness.

Stock markets generally started the week well as decent Chinese data and reopening in the country boosted sentiment around the world. This preview of weekly data looks at EURUSD and UKOIL ahead of inflation data from most major countries in the eurozone and various American releases while the G7’s summit continues.

Last week wasn’t especially active in monetary policy, with the Norges Bank calling for a two-step hike to 1.25% and the Banco de Mexico a three-step hike to 7.75%. In comments to the Senate, the Fed’s chair Jerome Powell reaffirmed commitment to tackling inflation with tighter policy. This week the only significant central bank for forex markets is the Riksbank on Thursday: the majority of expectations point to a half percent hike to 0.75%

Apart from inflation in the EU, the calendar this week also contains American income and spending, German jobs plus ISM manufacturing PMI and further industrial and manufacturing releases from China. Energy policy is obviously top of the agenda for the G7 in Germany this week, so for traders of oil in particular it’s likely to be helpful to watch the news closely.

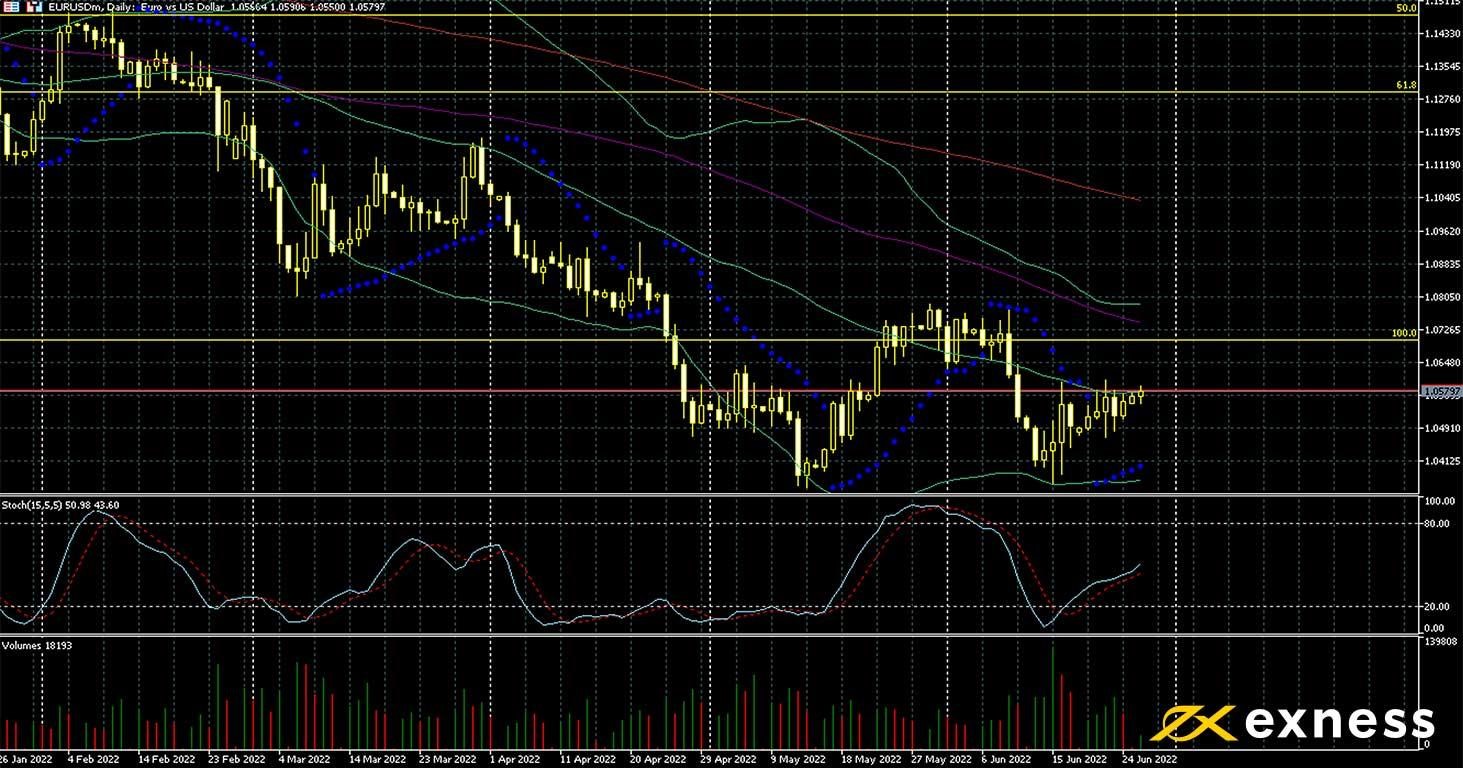

Euro-dollar, daily

The euro has recovered weakly against the dollar in the second half of June so far. Fundamentals still clearly favour the dollar, with the eurozone seemingly more vulnerable to recession, preventing the ECB from speeding up its tightening significantly, while the Fed has indicated that more 0.75% hikes are likely. Durable goods on 27 June was stronger than expected at 0.7%. Jerome Powell last week was unusually frank in asserting that recession is preferred over entrenched high inflation. However, central banks’ policies for the moment seem to be priced in, so the euro might receive further respite this week unless inflation is notably lower than expected.

On the chart, the picture is generally neutral aparts from moving averages. Volume is low so far this week and the slow stochastic is almost exactly neutral at just above 50. The 50 SMA is the main technical reference at the moment, with movement above there unlikely unless traders receive positive new information of some sort for the euro. Another test below $1.05 also doesn’t look likely this week unless there’s a real surprise from the data, though, so active trading seems to be preferred over the next few days, especially around inflation releases.

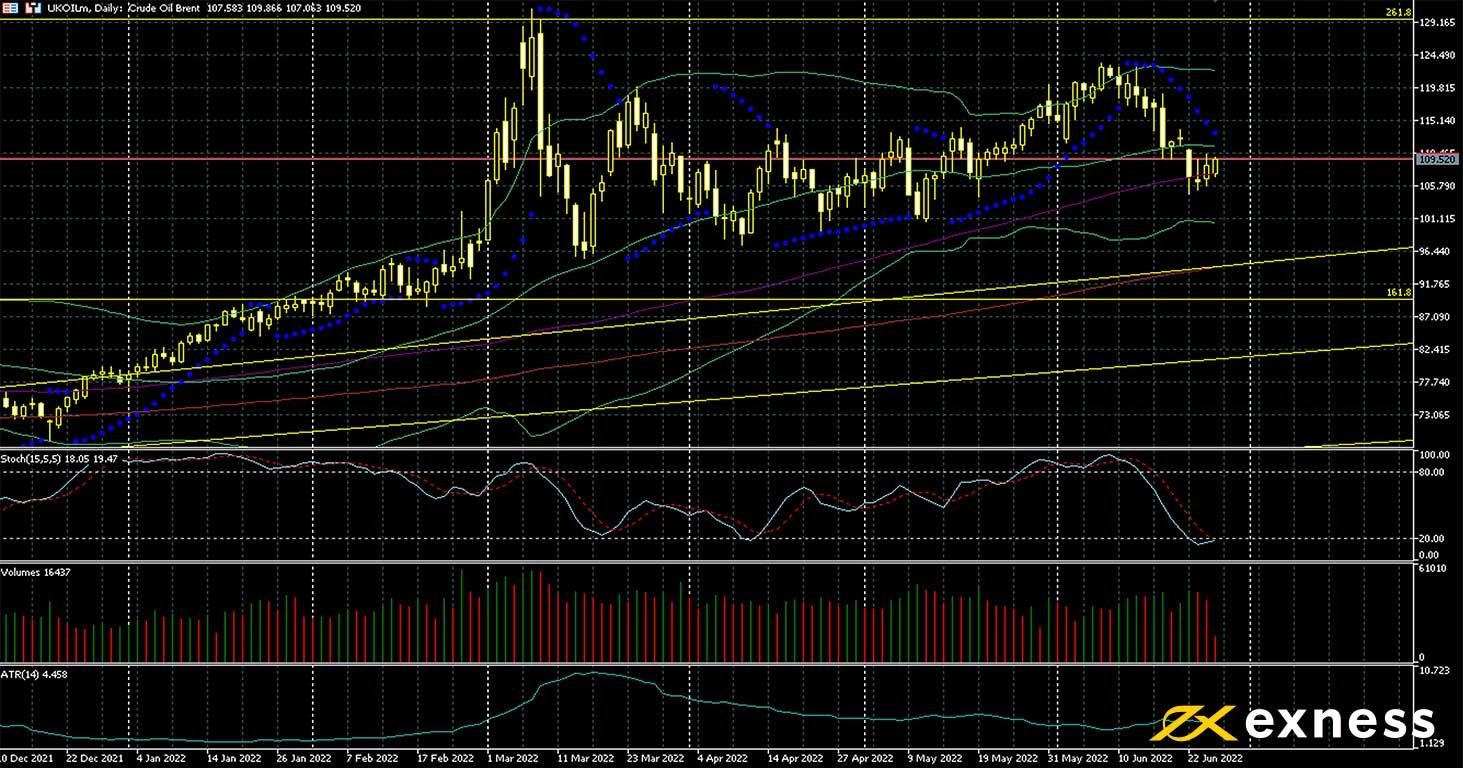

Crude oil has recovered so far this week as fears of recession while still present have moved somewhat out of the spotlight. Consistent with most of 2022 so far, supply remains tight with no indications of a significant expansion – the USA added only about 50 rigs in the whole of the second quarter so far. Discussions at the G7 of a cap on prices of Russian oil for export remain in focus, but there are questions about the practicality of enforcing this with restrictions on insurance and shipping.

The picture on the chart is overall somewhat positive, with the ongoing bounce starting around the 100 SMA and the slow stochastic still within the zone of selling saturation. Depending on this week’s stocks, the 50 SMA seems to be a possible resistance, so the price might hold within the value area pending new information from the G7, data, Russian exports or maybe even the resumption of US-Iranian talks next week. Wednesday sees a double release of the EIA’s stock data because of technical problems last week.

Key data this week

Bold indicates the most important releases for this symbol.

Tuesday 28 June

20:30 GMT: API crude oil stock change (24 June) – previous 5.61 million

Experienced writer and journalist, working in the global online trading sector, Steffy is the Editor of LeapRate. She has previous experience as a copywriter and has been with the company since January 2020. Steffy has a British and American Studies degree from St. Kliment Ochridski University in Sofia.