This article was submitted by Michael Stark, market analyst at Exness.

The recent selloff of bonds and rising yields has continued so far this week as participants increasingly price in an extended cycle of tightening monetary policy. Meanwhile oil has retreated somewhat since the end of last week as more major cities including Shanghai have entered lockdown. This preview of weekly data looks at UKOIL and EURUSD ahead of OPEC+’s meeting on Thursday and key job data from the USA on Friday.

Mexico, South Africa, Norway and Hungary all raised their base rates last week as expected. Traders have concentrated in the last few weeks on comments from senior members of the Fed explicitly allowing for a two-step rate hike: as of Monday 28 March, the likelihood of a hike to 0.75-1% on 4 May is about 70%. The next major central bank to meet is the Reserve Bank of Australia on 5 April.

The most important releases this week in regular data are of course the NFP and related job data from the USA on Friday afternoon GMT. Before these, though, markets are also looking at inflation from Germany and other major countries in the EU. If the current large movements in bond markets continue combined with oil and gold’s recent volatility, correlations might drive significant activity for many instruments even in the runup to Friday’s important figures.

Brent, daily

Brent has declined since last Thursday’s open as lockdowns were broadened across China and participants started to price in weaker demand, ignoring for the time being the lack of consensus on further sanctions against Russia. Markets generally seem to be reacting positively to reports at the start of the week that Turkey might host in-person talks between Ukrainian and Russian leaders.

The 261.8% Fibonacci extension around $129 remains in focus as the key resistance. A breakthrough above this remains highly unlikely unless there’s a significant change in fundamentals. $100 is the main psychological area below which might also drive a bounce if it were to be tested this week. With no signal of saturation and ATR declining, consolidation around $115 seems to be possible in the next few days.

OPEC+’s meeting on Thursday is likely to result in a continuation of recent increases in supply – at least in theory – although the cartel and its allies remain significantly below their targets for production. Traders will also probably monitor Baker Hughes’ rig count more closely than usual this week because of a possible peak being reached earlier this month around 530.

Key data this week

Bold indicates the most important releases for this symbol.

Tuesday 29 March

20:30 GMT: API crude oil stock change (25 March) – previous negative 4.28 million

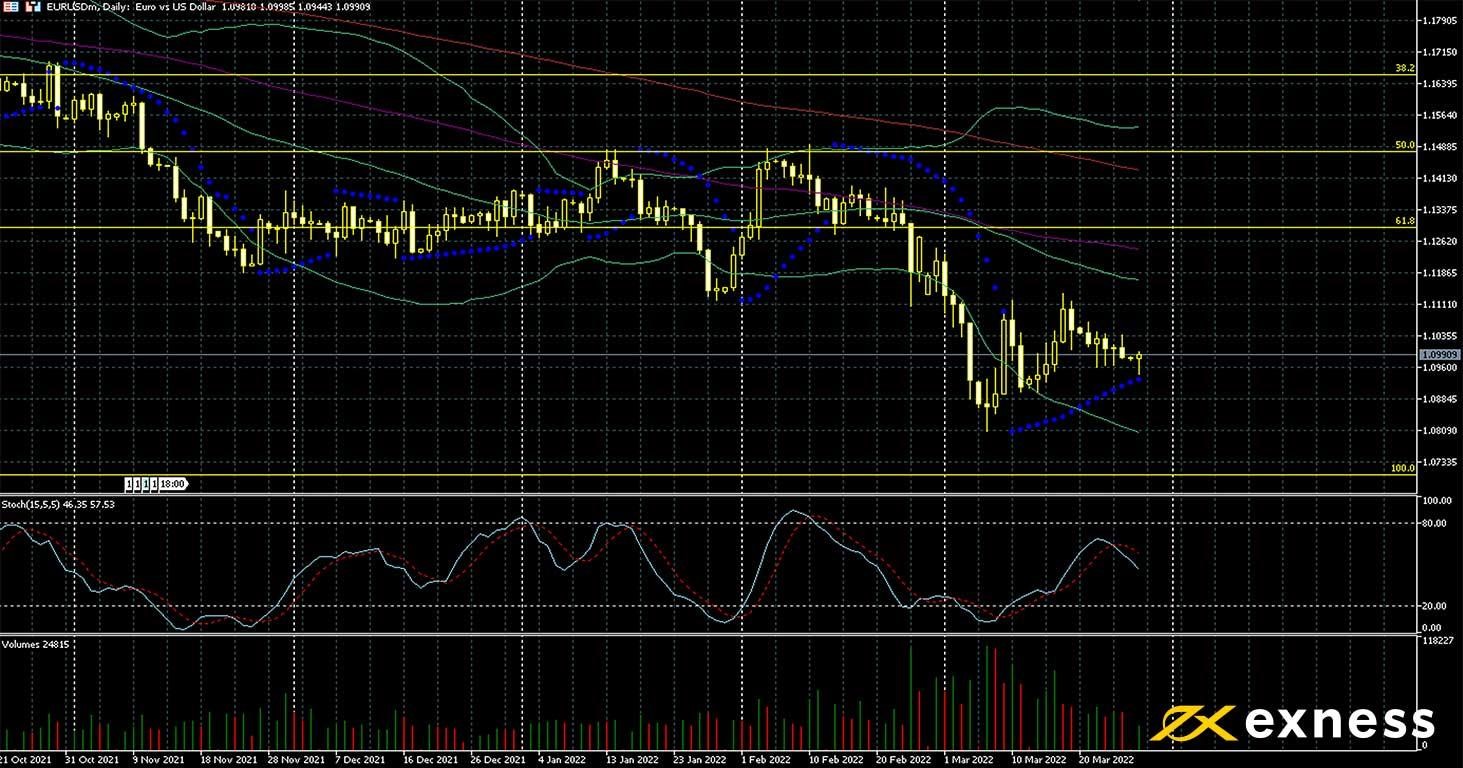

Euro-dollar recovered somewhat in the second half of March. On both sides, participants are starting to price in more serious tightening of monetary policy this year between a likely two-step hike by the Fed coming in May and the strong possibility of at least a small hike by the ECB by June. Flash eurozone annual inflation on Friday is expected to rise to a new record high of about 6.5%.

The recent consolidation seems to be driven less by fundamentals than what’s happening on the chart: sellers seem to have taken profits below $1.09, a 22-month low, with little demand for now to push the price lower. Although there’s no oversold signal and moving averages are successively above each other and the price, volume has tailed off in the last fortnight. Traditionally, new sellers from here would prefer to wait for a bounce before joining the downtrend.

Such a bounce might appear from Thursday or Friday depending on the reaction to the various releases on those days. Even in the case of a stronger shift in fundamentals to the dollar’s favour, new lows seem unlikely in the immediate future.

Key data this week

Bold indicates the most important releases for this symbol.

Experienced writer and journalist, working in the global online trading sector, Steffy is the Editor of LeapRate. She has previous experience as a copywriter and has been with the company since January 2020. Steffy has a British and American Studies degree from St. Kliment Ochridski University in Sofia.