This article was submitted by Michael Stark, market analyst at Exness.

Last week’s very high annual inflation from the USA, with both the core and non-core figures posting 30-year records, has brought inflation sharply back into view for most participants in the markets. Meanwhile American consumer sentiment last week reached a new 12-year low. Complacency in markets remains high, though, with generally strong Chinese data kicking off this week and the VIX around 17. This preview of weekly data looks at CADJPY and GBPZAR ahead of important inflation data in the middle of the week.

There was no real activity among central banks last week, but comments this morning from the American Secretary of the Treasury Janet Yellen that inflation is unlikely to decline significantly until the second half of 2022 are important. These represent a challenge to the narrative to which the Fed still adheres that the situation is ‘transitory’. Regionally important events this week include meetings of the Central Bank of the Republic of Turkey and the South African Reserve Bank on Thursday. The CBRT is expected to cut its one-week repo rate by 1% to 15%.

Tuesday morning’s key release is the claimant count change from the UK. Other important regular data this week include inflation from the UK, Canada, Japan, South Africa and some countries in the eurozone. The focus in these releases is likely to be on how they might affect monetary policy in the relevant countries because it increasingly seems that most central banks will have to act sooner rather than later in the face of sharply rising inflation.

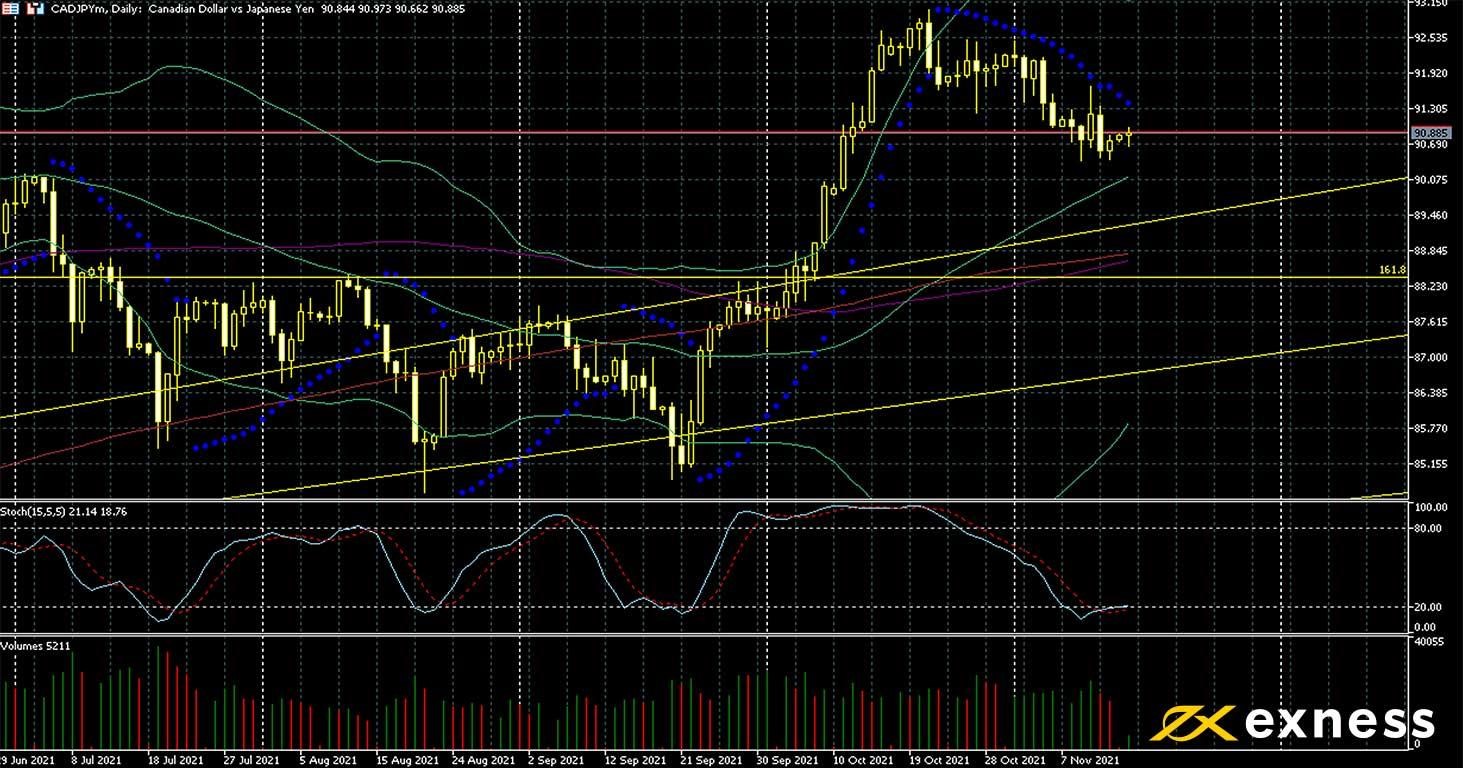

Canadian dollar-yen, daily

The loonie’s traditional correlation with crude oil has been fairly reliable since summer, with CAD mirroring the commodity’s gains in many of its pairs. Dovish comments on Monday morning from Haruhiko Kuroda, the governor of the Bank of Japan, that loose policy will be maintained and that inflation is unlikely to rise to 2% until later next year have dented sentiment on the yen somewhat.

September and October’s large upward movement seemed to be somewhat excessive, with the consolidation ongoing, but more gains are likely based on TA. ¥90 is an important psychological area that might trigger a bounce, and the 50 SMA slightly above this could also function as a support. The 100 SMA seems to be about to golden cross the 200, while recent emergence from oversold would suggest a possible retest of the latest high.

This week’s data are likely to introduce some volatility, especially around Canadian annual inflation on Wednesday. Balance of trade from Canada on Tuesday evening is also an important release. Conversely, a possible ongoing decline by oil could mean headwinds for the Canadian dollar here as in other pairs.

Key data this week

Bold indicates the most important releases for this symbol.

Tuesday 16 November

50 GMT: Japanese balance of trade (October) – consensus negative ¥310 billion, previous negative ¥622.8 billion

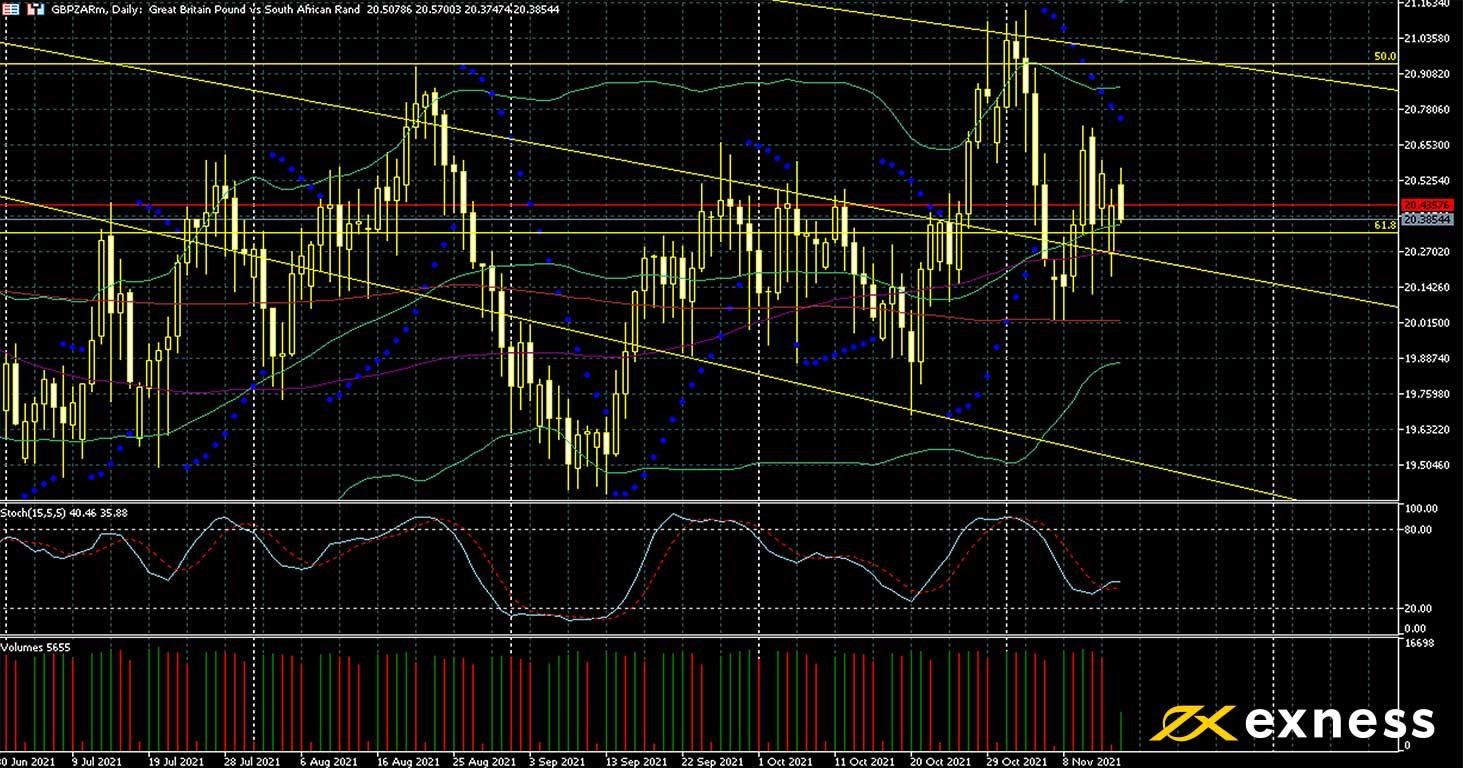

Pound-rand has been in a sideways trend although with some periods of higher volatility since about this time last year. The South African government’s downward revisions of forecasts for its budget deficit and debts have helped to increase confidence, while the BoE’s reluctance to tighten policy in defiance of expectations this month has also contributed to the pound’s recent losses.

There doesn’t seem to be much scope for more losses in the immediate future based on TA, though. With the price approaching the value area between the 50 and 100 SMAs, there would probably need to be significant new selling to push beyond here, and that’s unlikely in the runup to the SARB’s meeting on Thursday. In the short term, some volatility seems favourable, especially around this week’s key data, but direction might become clearer from Thursday afternoon.

The Bank of England has stressed that it will look closely at data in the next few weeks to decide whether it will raise the bank rate in December. In practice, this means that inflation is the main figure in view this week, but claimant count change is also a key release because it indicates the possible health of the job market.

Key data this week

Bold indicates the most important releases for this symbol.

Experienced writer and journalist, working in the global online trading sector, Steffy is the Editor of LeapRate. She has previous experience as a copywriter and has been with the company since January 2020. Steffy has a British and American Studies degree from St. Kliment Ochridski University in Sofia.