This article was submitted by Michael Stark, market analyst at Exness.

Riskier instruments such as shares and cryptocurrencies generally recovered slightly on Monday in a slow day of trading with the USA on holiday. Since the middle of last week and the Fed’s triple hike, nervousness in many markets has been quite high. This preview of weekly data looks at GBPNZD and USDCAD ahead of data on inflation around the world.

The Fed delivered last week with a hike of 0.75% of the funds rate, taking it to 1.5-1.75%, reiterating its firm commitment to tackling inflation. According to CME FedWatch Tool, the chance of another triple hike next month is more than 99%. The dollar didn’t make significant ongoing gains in the aftermath given that a triple hike had been widely priced in since the Monday of that week and, as noted below, the greenback remains close to a 20-year high.

The Bank of England also hiked its rate last week although by only a quarter of a percent; the pound briefly found support in the aftermath. Finally among relevant central banks, the Swiss National Bank started tightening last week with a two-step hike. This week is less active in monetary policy, but markets are expecting Norway and Mexico to hike their rates on Thursday.

Inflation is the focus of regular data this week, with the UK, Canada and Japan all due to report on the rate of prices’ increases. Markets also await New Zealand’s balance of trade late on Tuesday night GMT. This is quite an active week of data for some countries such as the UK, while in the USA it’s not especially busy, so cryptocurrencies and indices might move more on correlations and expectations for monetary policy in the next few days.

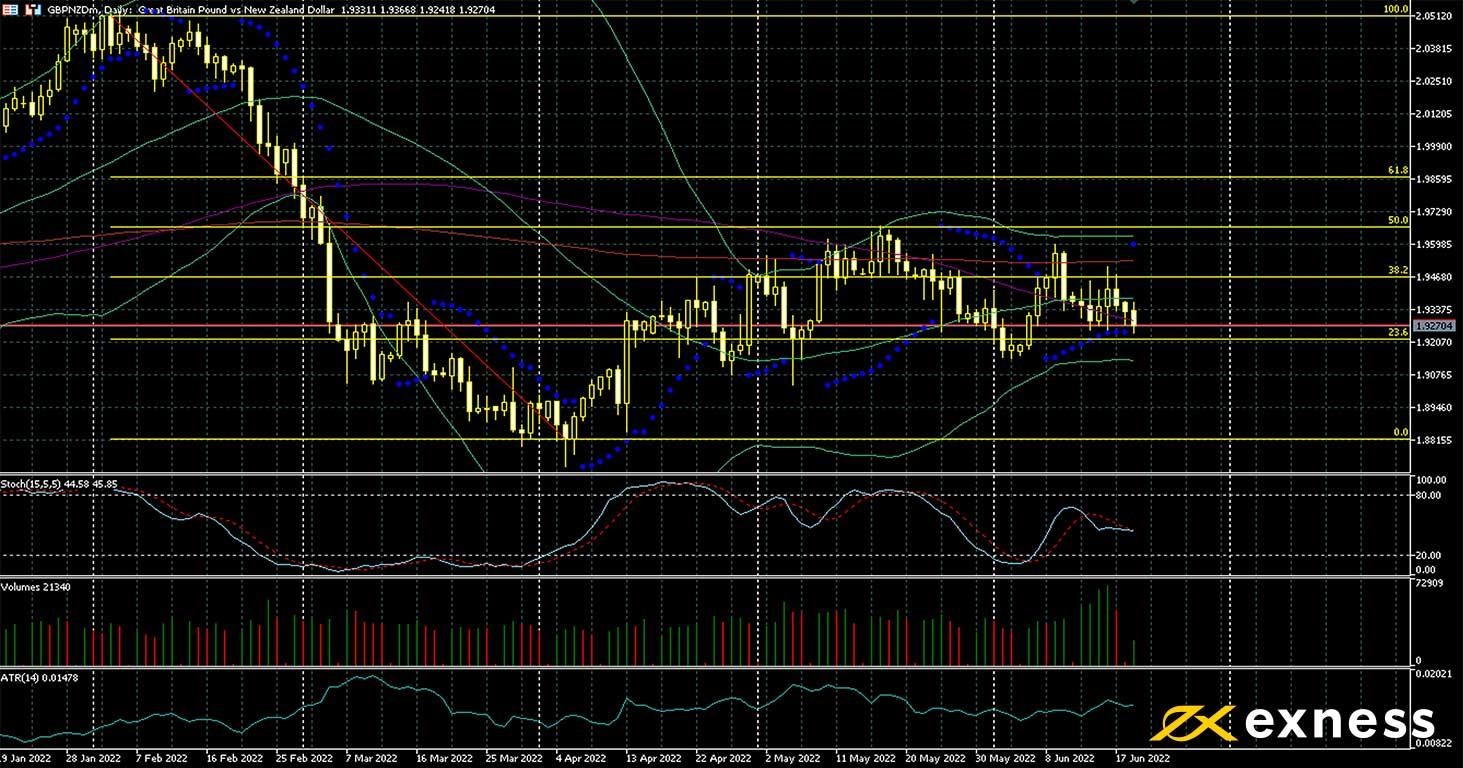

Pound-Kiwi dollar, daily

The pound has generally performed poorly so far this week as fears of recession in the UK increase and a national rail strike began on Tuesday. The Bank of England hiked its rate by 0.25% last week, but participants seem to view this as not enough: inflation in the UK remains at a 40-year high and is expected to move above 10% in the third quarter. The Reserve Bank of New Zealand has been somewhat more hawkish than the BoE but the Kiwi dollar has also been weak against many currencies in the last few weeks. As a trade-sensitive currency, it typically does poorly when the outlook for major economies worsens as it has this quarter.

There is no very clear signal from the chart except for the price being below all three of the 50, 100 and 200 simple moving averages, suggesting movement lower. The slow stochastic is close to neutral and there has been no significant change in ATR in June so far. In this context of no clear trend, the volume of British data this week and Kiwi balance of trade might provide short-term momentum-based opportunities in both directions throughout the week.

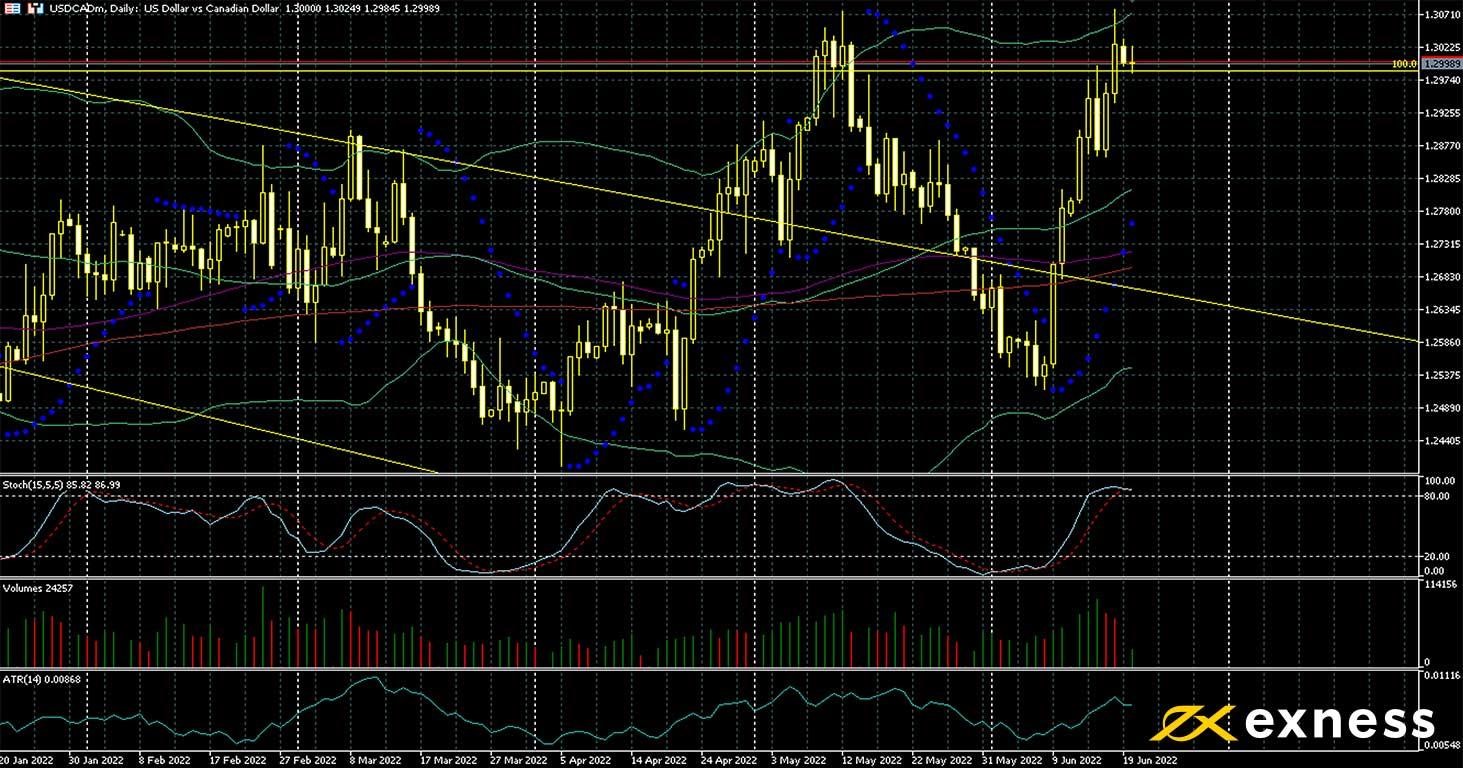

The greenback reached a 20-year high last week as stronger American inflation the week before propelled expectations of a triple hike by the Fed. This was delivered, so the dollar has held near recent highs in most of its major pairs. Increasing warnings of recession are a negative factor for most major, advanced economies, not just the USA, and nearly every country except Japan is likely to see inflation above 2% for several years. In Canada, inflation is not quite as concerned as south of the border, but the Bank of Canada is still expected to call for a triple hike at its upcoming meeting on 14 July. Recent job data from Canada were also strong.

The technical picture seems to align with fundamentals in pointing to a possible move down. C$1.30 is a crucial psychological area aligning with the 100% weekly Fibonacci retracement and an 18-month high just above. The slow stochastic gives a clear overbought signal, so these factors together make it difficult to envision a sustained movement further up unless there’s a notable shift in expectations for monetary policy. This week’s clear focus is on Canadian inflation on Wednesday. If the reading is higher than expected there would be strong support for the BoC’s hawkish intentions. Markets will also look at comments from Jerome Powell on Wednesday and Thursday.

Key data this week

Bold indicates the most important releases for this symbol.

Experienced writer and journalist, working in the global online trading sector, Steffy is the Editor of LeapRate. She has previous experience as a copywriter and has been with the company since January 2020. Steffy has a British and American Studies degree from St. Kliment Ochridski University in Sofia.