This article was submitted by Michael Stark, market analyst at Exness.

Asian and European shares mostly started the week on the front foot, with oil also gaining from today’s opening. Somewhat weaker PMI from China and lower than expected German retail sales haven’t affected markets negatively so far. This is a very important week of data and for central banks: this preview of weekly data looks at AUDUSD and GBPNZD.

There were no significant changes in monetary policy last week, with the European Central Bank’s meeting leading to gains by the euro initially followed by sharp losses on Friday. This week sees three major central banks meet: the Reserve Bank of Australia, the Bank of England and most importantly the Federal Open Market Committee. None of these are likely to confirm the timing of significant changes to policy, but hints on this are possible during press conferences, and each bank’s view of the economy is likely to affect sentiment. The National Bank of Poland is expected to increase its reference rate to 0.75%, and the Norges Bank will also meet on Thursday.

Regular data this week have their focus on Friday’s non-farm payrolls and American unemployment rate. Also critical are balance of trade from Australia, Canada and the USA, while some participants will monitor job data from New Zealand on Tuesday night. Earnings season in the USA is nearly over, but a number of large companies will still report this week. Overall, activity is likely to be quite high in markets around central banks’ meetings and the NFP over the next few days, so short-term opportunities in both directions are likely for many forex pairs and pairs with metals.

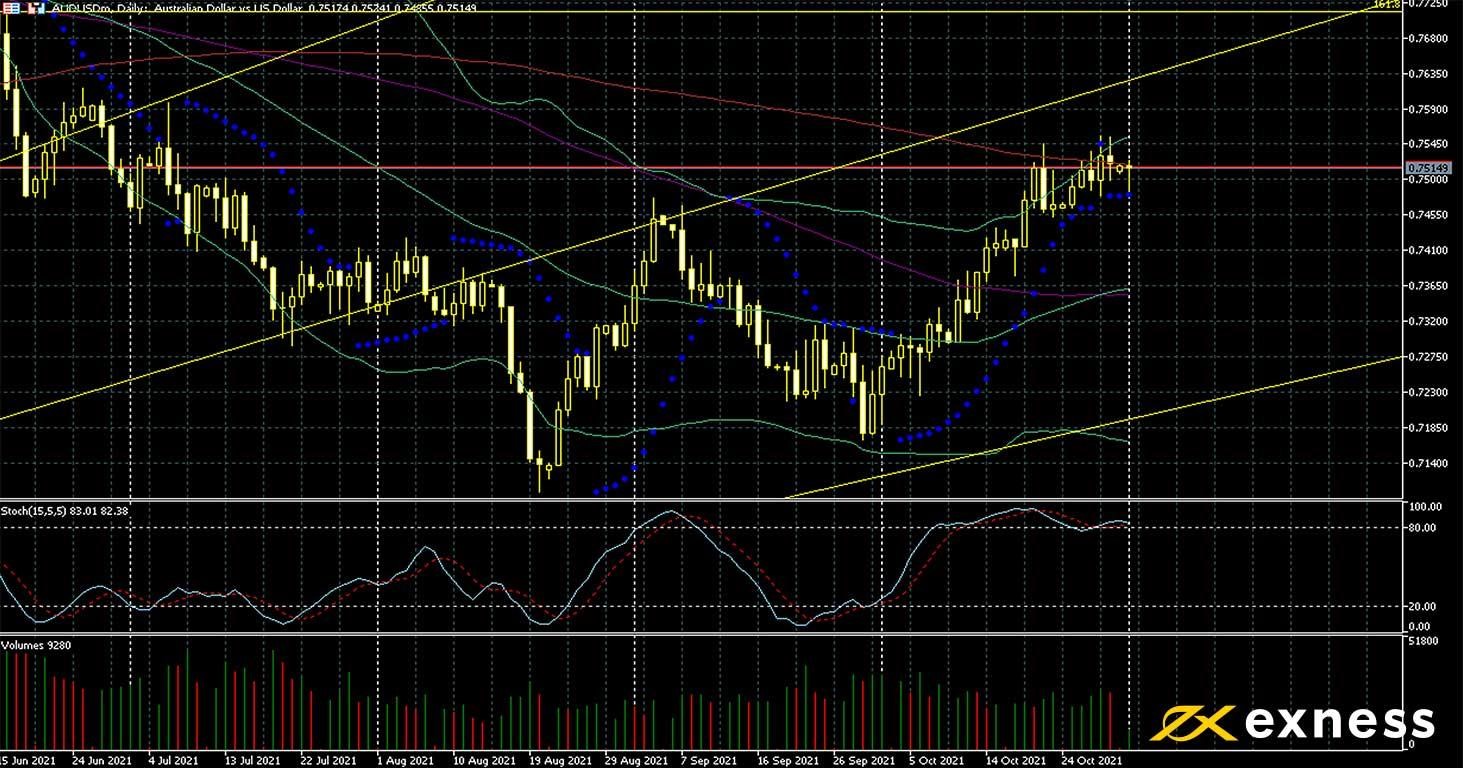

Australian dollar-US dollar, daily

Strong gains by various ores and industrial commodities since summer have boosted sentiment on the Aussie dollar given the key role that exports of these play in Australia’s economy. Speculation on the direction of monetary policy on both sides of this symbol has been a key factor in the last few weeks. While a change to the cash rate or funds rate this week is very unlikely, the RBA is widely expected to signal earlier hikes and abandon its target of 0.1% for yields of government bonds expiring in April 2024. Meanwhile the Fed is also expected to announce more details of tapering soon.

AUDUSD’s uptrend seems to be resuming at the time of writing on the daily chart considering highs on 3 September and 20 and 28 October. The 50 SMA from Bands is about to complete a golden cross above the 100 SMA, but the 200 SMA is still an important resistance which the price is currently testing. Between this and overbought based on the slow stochastic (15, 5, 5), a sustained round of gains this week doesn’t seem likely unless the news and data strongly favour the Aussie dollar.

30 GMT: American annual average hourly earnings (October) – consensus 4.9%, previous 4.6%

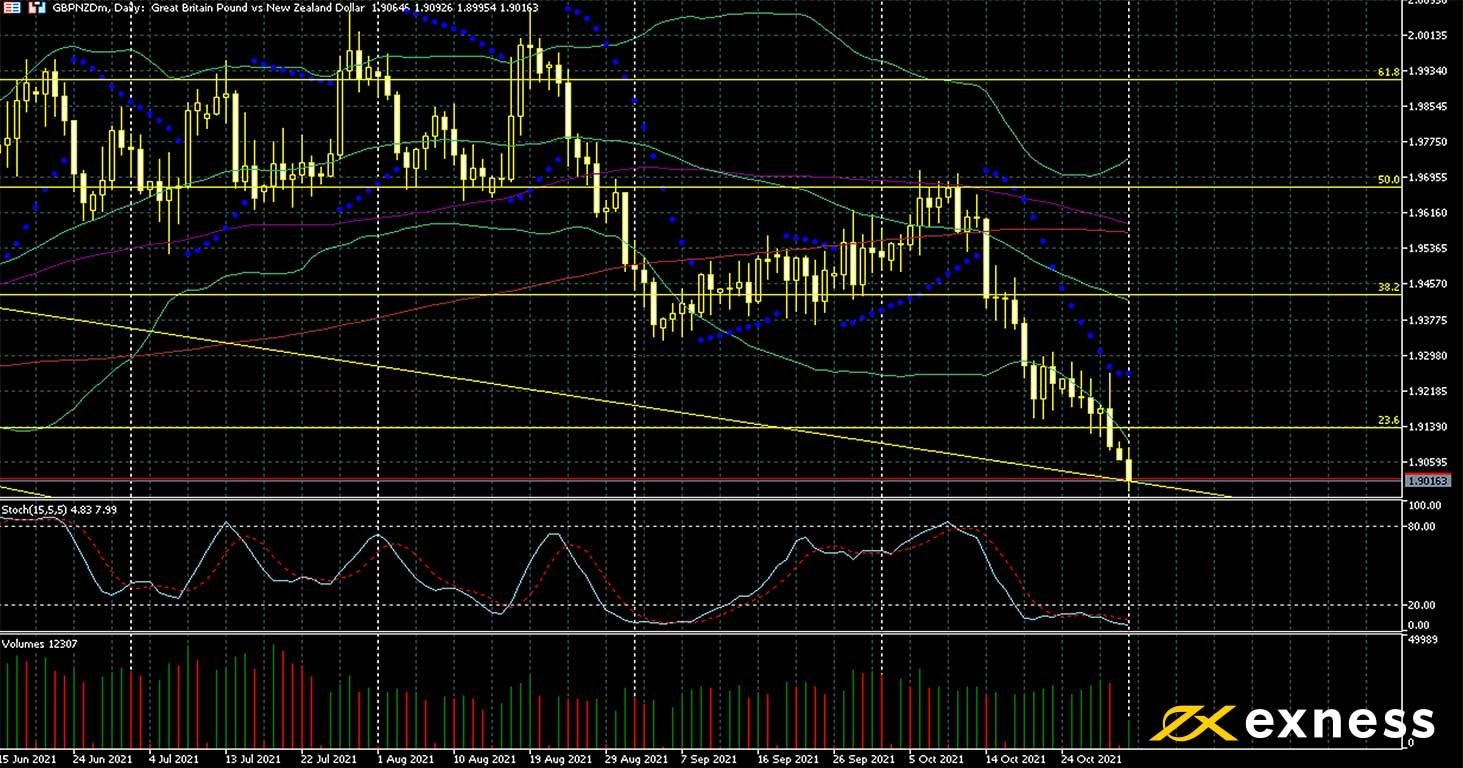

Pound sterling-New Zealand dollar, daily

The pound declined sharply last month against the Kiwi dollar as the Reserve Bank of New Zealand hiked its cash rate on 6 October, the first major central bank to do so since the ‘race to zero’ last year, while the Bank of England is now perceived to be somewhat less hawkish than it had seemed in August and September. Projections for the British economy are fairly strong, with expected growth for the full year of 2021 revised higher and unemployment further down according to Rishi Sunak; however, the current standoff with France over fishing rights in the Channel has dented sentiment on the pound somewhat. The Reserve Bank of New Zealand is widely expected to hike its rate again this month.

The 61.8% zone of the weekly Fibonacci fan around $1.90 seems to be a strong support from which a small intraday bounce was observed on Monday around noon GMT. The current rate just above that area is a low of about eight months, and with the stochastic clearly oversold since the middle of October, a bounce seems to be possible this week if the data and news from the BoE align. The other main possibility is another leg down with no clear support until $1.87, December 2020’s low. Volatility is very likely to be high this week but the releases could also determine the extent and timing of possible ongoing losses.

Key data this week

Bold indicates the most important releases for this symbol.

Experienced writer and journalist, working in the global online trading sector, Steffy is the Editor of LeapRate. She has previous experience as a copywriter and has been with the company since January 2020. Steffy has a British and American Studies degree from St. Kliment Ochridski University in Sofia.