This article was submitted by Michael Stark, market analyst at Exness.

Many European shares began the new year with gains as sentiment has remained generally strong and markets still seem to be perceiving the threat from omicron as overblown. After a fairly slow start to the year of trading as usual, activity is likely to pick up towards the middle of the week around the FOMC’s latest minutes and ahead of European inflation and the NFP on Friday.

Central banks were generally inactive last week as is usual for the week between Christmas and new year. Markets have mostly priced in faster and stronger tapering of quantitative easing this year in most major economies, so focus is likely to remain on central banks and inflation, especially the Federal Open Market Committee’s latest minutes on Wednesday night and inflation from the eurozone on Friday. The next critical meeting is the Fed on 26 January.

Apart from the releases noted above, big regular data this week such as balance of trade from Germany and the USA on Thursday and Friday respectively might drive more movement for euro-dollar and other widely traded instruments like possibly gold. Before the key releases, many instruments are likely to consolidate amid relatively low volume as participants build positions gradually.

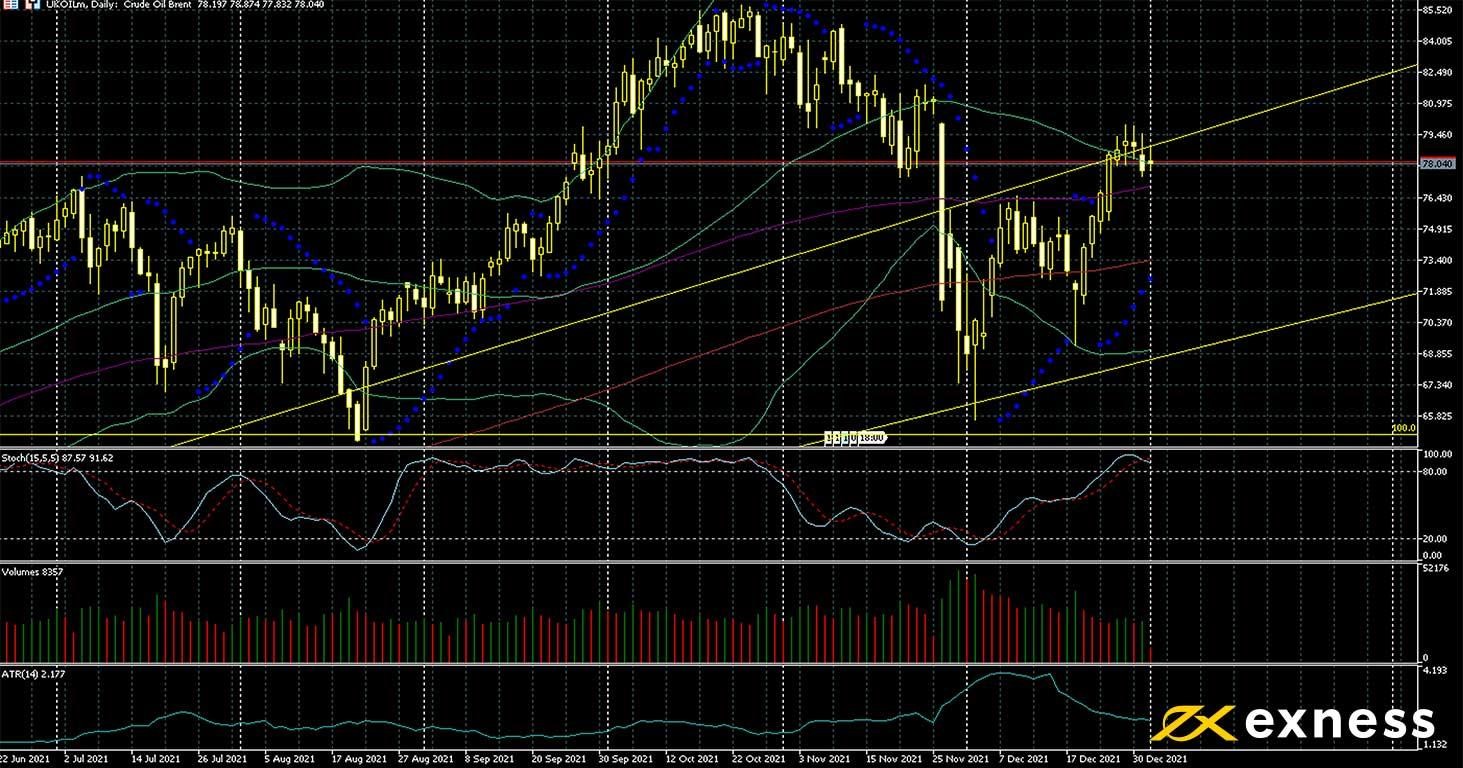

Brent, daily

Oil has bounced quite strongly since the week before Christmas as fears over omicron’s possible hit to demand appear to have been unfounded so far. OPEC+’s virtual meeting on Tuesday is expected to result in an increase of 400,000 barrels daily in February as planned. The cartel and its allies’ apparent confidence in the face of steadily rising American supply has boosted sentiment, while recent disruption of supply from Libya has also been a positive for the price.

From a technical point of view, a clear move back above $80 seems to be unlikely as of now given this area’s importance as a psychological resistance and buying saturation based on the slow stochastic. ATR of around $2.20 is now about half the peak in December, though, so a retest of $80 seems very likely even if a round of losses follows. A range between around $70 and $80 might be established over the next few days if there’s no major change in sentiment or patterns in data with the value area between the 100 and 200 SMAs its focus.

As an industrial commodity, oil generally isn’t very sensitive to monetary policy and inflation, more the early stages of an inflationary cycle. However, sentiment around OPEC+’s meeting on Tuesday is likely to be very important, while as usual traders will also watch regular stock data from the USA plus Baker Hughes’ rig count on Friday.

Key data this week

Bold indicates the most important releases for this symbol.

Tuesday 4 January

all day: meeting of OPEC+

30 GMT: API crude oil stock change (31 December) – previous negative 3.09 million

The pound is now at its highest in about two months against most major currencies having recovered from annual lows on 20 December. Key drivers behind recent gains are the avoidance so far of additional restrictions on movement or activity after increasing numbers of cases of omicron in the UK and of course the Bank of England’s decision to hike its bank rate last month to 0.25% by a fairly large majority.

Markets are currently pricing in three or four more hikes this year by the BoE. Growing divergence in monetary policy is the key reason for the yen’s losses here with inflation in Japan still significantly below the target of 2%, but the Bank of Japan signalled at its last meeting that it plans to unwind QE to pre-pandemic levels by the end of April 2022.

On the chart, it looks like the pound might be due a consolidation given overbought based on the slow stochastic and the speed of gains since late last month. The main technical reference is the 161.8% weekly Fibonacci extension area around ¥153.60. A break significantly below this isn’t likely in the near future given the three moving averages slightly below ¥152. To the upside and in the longer term, the target remains the psychological area of ¥160, which would be a high of about six years. However, the latest highs around ¥158.10 might be difficult to breach.

There isn’t any critical data for pound-yen itself this week, but the FOMC’s minutes on Wednesday night might be important because they could emphasise the gulf between the BoJ and other major central banks including the BoE. Equally, the pound as a more cyclical and trade-sensitive currency can behave similarly to the dollar against havens around the NFP.

Experienced writer and journalist, working in the global online trading sector, Steffy is the Editor of LeapRate. She has previous experience as a copywriter and has been with the company since January 2020. Steffy has a British and American Studies degree from St. Kliment Ochridski University in Sofia.