This article was submitted by Michael Stark, market analyst at Exness.

European shares have performed well so far this week as markets generally react positively to data in the eurozone, while commodities have posted some gains. The key event this week is the meeting and press conference of the Federal Open Market Committee tomorrow night. This preview of weekly data looks at USDCAD and NZDJPY.

Last week’s significant event in monetary policy was the Central Bank of the Russian Federation’s rate hike of 0.5% to 5.5%, double the 0.25% expected. Tomorrow evening’s meeting of the FOMC is the key event this week, while some traders will also monitor snippets of news from the Bank of Japan’s meeting early on Friday morning.

The focus of regular data to come this week is on British and Canadian inflation tomorrow. Japanese balance of trade late tonight GMT and inflation on Thursday morning are likely to be important for the yen. Regionally important releases include New Zealand’s GDP data tomorrow night plus Australian employment releases on Thursday morning.

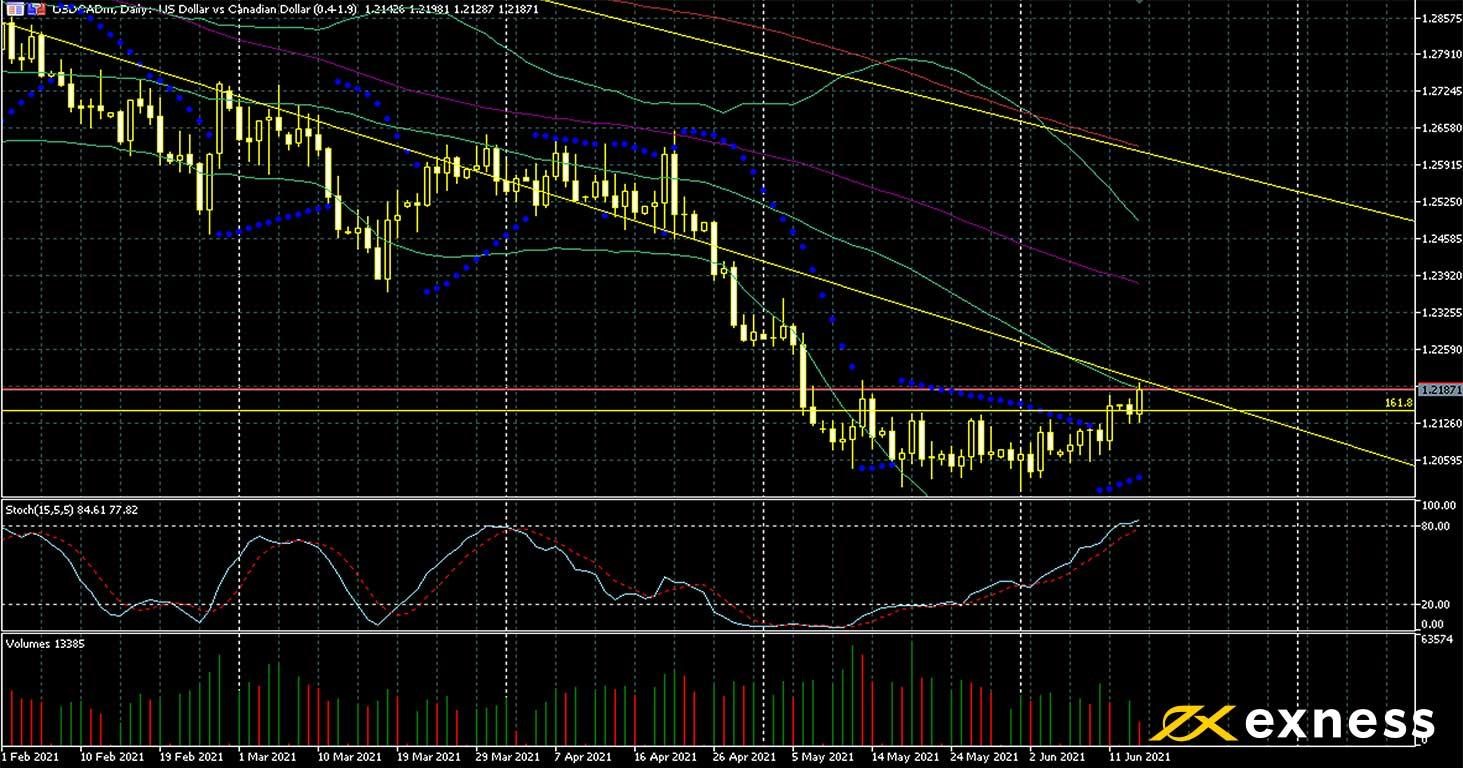

US dollar-Canadian dollar, daily

The greenback has bounced slightly from four-year lows against the loonie so far this week. The Bank of Canada left rates on hold at its last meeting as universally expected while stressing that extraordinary support from monetary policy would be needed for some time to come.

However, the BoC has started to taper its purchases of bonds, the first major central bank to do so. The next announcement of slow winding down is expected on 14 July. Oil meanwhile has supported the loonie over the last few days, with American light oil rising to about $70.50 today.

The 161.8% weekly Fibonacci extension area based on the US dollar’s gains in March last year remains the key technical reference. As of now, a clear push below this zone still looks unlikely. Conversely, a movement above the 50 SMA from Bands, which seems likely in the near future, probably won’t signal a reversal. Instead, ranging movement over the next few weeks seems to be likely unless there’s a significant surprise from the Fed tomorrow night.

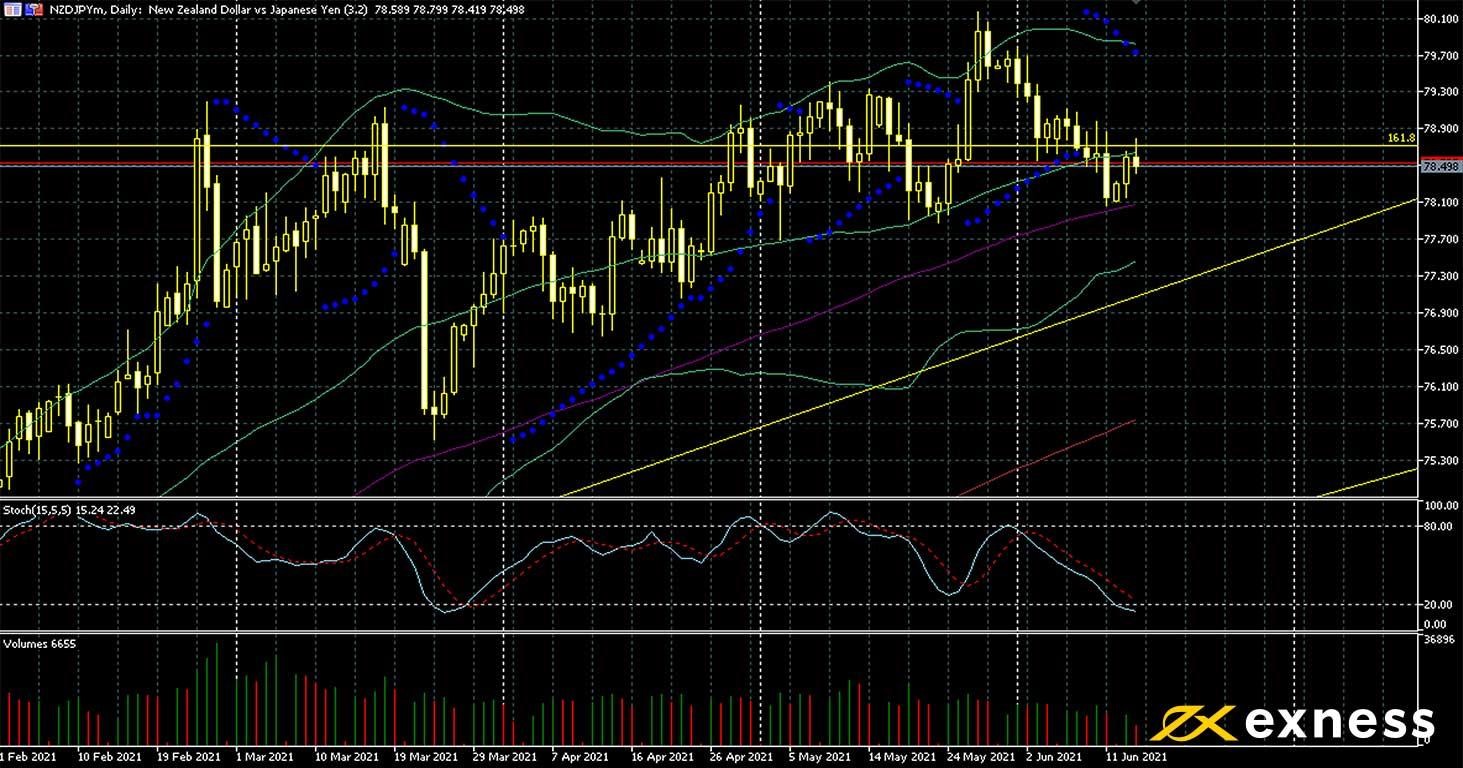

The Reserve Bank of New Zealand’s signalling of a likely rate hike in the second half of next year makes it – relatively speaking – among the more hawkish central banks at the moment, and with the current stability in trade fundamental factors align in favour of the Kiwi dollar. Ongoing border controls are a negative for NZD.

Momentum here has decreased over the last few weeks, with price following the 50 SMA from Bands more closely and testing the 100 SMA late last week. However, the slow stochastic signals oversold. The key data this week for NZDJPY are Kiwi GDP figures tomorrow night. The last quarterly and annual figures showed unexpected drops, but this seems unlikely to happen again tomorrow. The Fed’s meeting tomorrow might also generate volatility for this symbol as it might inform general sentiment in markets.

Key data this week

Bold indicates the most important releases for this symbol.

Tuesday 15 June

45 GMT: New Zealand current account (Q1) – consensus negative NZ$2.23 billion, previous negative NZ$2.7 billion

50 GMT: Japanese balance of trade (May) – consensus negative ¥91.2 billion, previous ¥255.3 billion

Wednesday 16 June

45 GMT: New Zealand annual GDP growth (Q1) – consensus 0.9%, previous negative 0.9%

45 GMT: New Zealand quarterly GDP growth (Q1) – consensus 0.5%, previous negative 1%

Experienced writer and journalist, working in the global online trading sector, Steffy is the Editor of LeapRate. She has previous experience as a copywriter and has been with the company since January 2020. Steffy has a British and American Studies degree from St. Kliment Ochridski University in Sofia.