This article was submitted by Michael Stark, market analyst at Exness.

European stock markets have generally started the week cautiously after sharp declines in Chinese shares. Regulatory tightening in China, rising numbers of covid-19 cases around the world and to some extent a return to focus on inflation have affected today’s movements so far. This preview of weekly data takes a look at XAUUSD and EURCAD ahead of this week’s key news, the FOMC’s statement and Canadian inflation.

The surprise in monetary policy last week was the Central Bank of the Russian Federation’s hike of its key rate by a full percent, double what had been expected. Markets still reacted negatively though with USDRUB gapping up over the weekend to trade at about ₽74 at noon GMT on Monday. The focus this week is on the Federal Open Market Committee’s statement and subsequent press conference on Wednesday night GMT. As at previous meetings, traders are mainly concerned with specific details about the timing of tightening, although very small rate hikes within the current range of nil to 0.25% are also in view.

This week’s most important regular data include Canadian inflation, German sentiment and American consumer spending. Stock markets and many major currencies are likely to be quite active as earnings season continues, with various big companies such as Tesla, AMD, Google, Microsoft, Apple, Facebook, Amazon and a large number of others due to report Q2’s results this week.

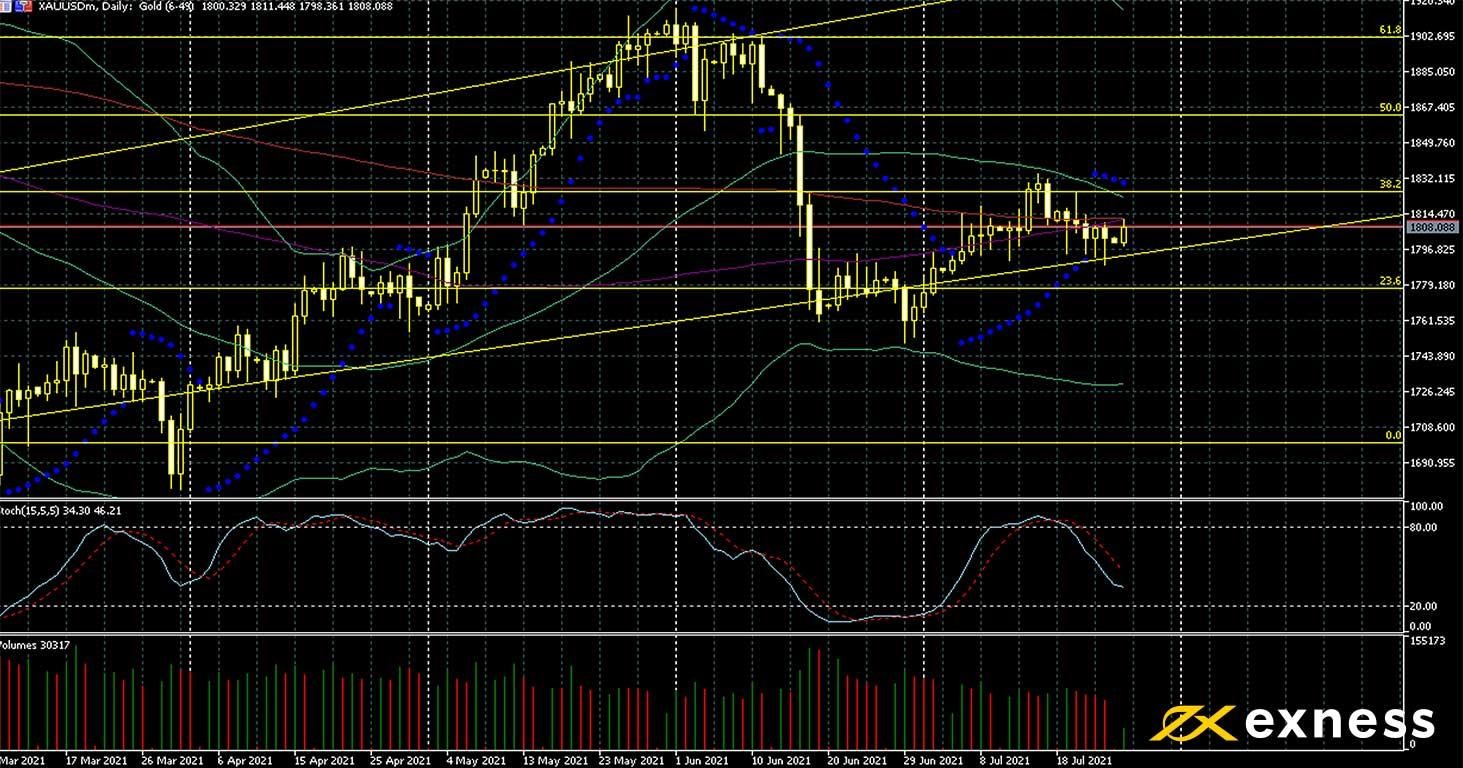

Gold-dollar, daily

Gold made modest gains this morning GMT as nervousness in markets increased somewhat although the dollar has held close to recent highs. A rising number of cases of covid-19 in various major economies due mainly to the more infectious Delta variant have dented ‘risk on’ and appear to give the yellow metal room to move up again despite continuing expectations of relatively swift monetary tightening in the USA.

The 61.8% area of the weekly Fibonacci fan seems to be quite a strong dynamic support from which a bounce might be expected, but the bunching of the 50, 100 and 200 SMAs might make significant movement upward from here a challenge. 15 July’s high around $1,834 seems to be the main static resistance in view for now.

Activity for XAUUSD probably won’t be very strong in the runup to Wednesday’s statement and press conference of the FOMC, but movements are likely to pick up from then. The key question remains how confident the Committee will be in the face of significant hesitancy among many individuals to vaccinate and the impact of Delta. Next week’s NFP is also a critical release.

Key data this week

Bold indicates the most important releases for this symbol.

30 GMT: American personal spending (June) – consensus 0.7%, previous nil

30 GMT: American personal income (June) – consensus negative 0.3%, previous negative 2%

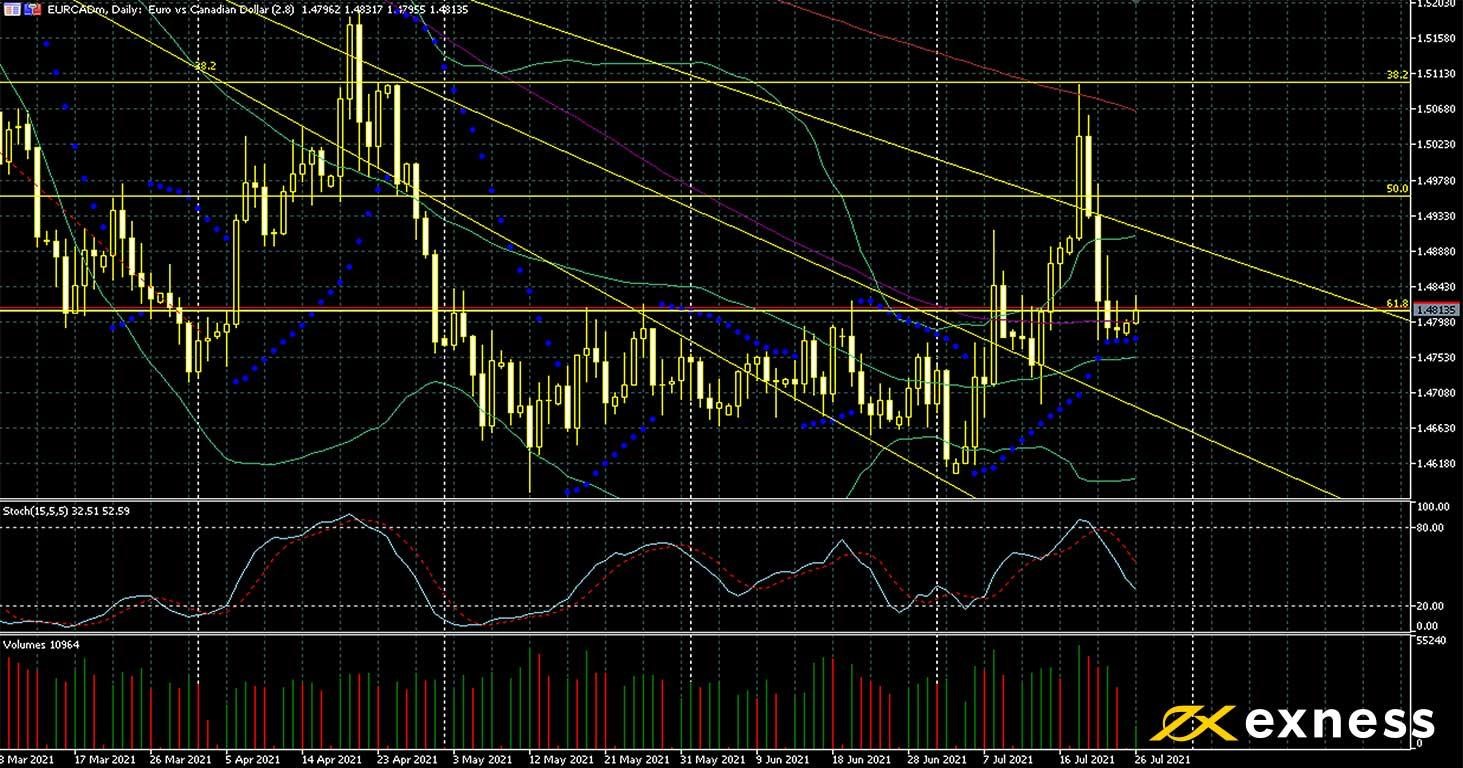

Euro-Canadian dollar, daily

Euro-loonie has been more volatile than usual over the last fortnight as oil declined sharply before a fairly strong recovery since Wednesday. The ECB remains among the more dovish central banks, while Canada’s economy probably stands to take the bigger hit if risk sentiment declines further on possible rising hospitalisations due to Delta.

The Canadian dollar’s direct correlation with crude oil has been very strong in July so far, so above and beyond TA this is a key factor likely to drive the price of EURCAD in the near future. With the price having moved above the 100 SMA and generally held there since last week, another round of losses probably isn’t favourable unless crude shoots up quite strongly, whether as a result of changing sentiment or good stock data on Wednesday. The 50% weekly Fibonacci retracement area might be an important resistance this week.

Wednesday’s German sentiment and Canadian annual inflation are the key figures to watch over the next few days. However, most markets are likely to be quite volatile around the FOMC’s statement on Wednesday night since many participants will infer reactions from other central banks like the ECB and BoC.

Key data this week

Bold indicates the most important releases for this symbol.

Experienced writer and journalist, working in the global online trading sector, Steffy is the Editor of LeapRate. She has previous experience as a copywriter and has been with the company since January 2020. Steffy has a British and American Studies degree from St. Kliment Ochridski University in Sofia.