Liquidity in the fixed income market has been declining over the past decade, but new matchmaking technologies can increase efficiency, deal flow and lower costs for all participants in primary bond markets.

The following post is courtesy of Overbond, the end-to-end platform for bond origination, set to publish a whitepaper on the transformation of the bond markets.

Over the past decade, liquidity has decreased throughout the bond market. In the past, “if average market liquidity was a 5 on a scale of 1 to 10, today’s markets might be something like a 3 or 3½,” said Tony Rodriquez, co-head of fixed income at Nuveen Asset Management, in a 2014 interview with the Wall Street Journal. Liquidity has continued on a downward trend as the difficulty of trading bonds increases. Electronic trading, on the other hand, is on the rise—evidence of a market that is increasingly interested in automation and digitization becoming integral parts of their workflows.

In a healthy and prosperous economy, a well-functioning and highly efficient primary bond market is a necessity, providing efficient allocations of capital to fund expansion and major investments. As it stands, though, the bond market is made up of many moving parts, all of which are in some senses competing, and in some senses working together, to create an agreeable outcome.

Current Status of the Canadian Fixed Income Market

To understand the way that digitization and automation technologies can affect change in the bond market, it is first necessary to understand the dynamics of the existing system.

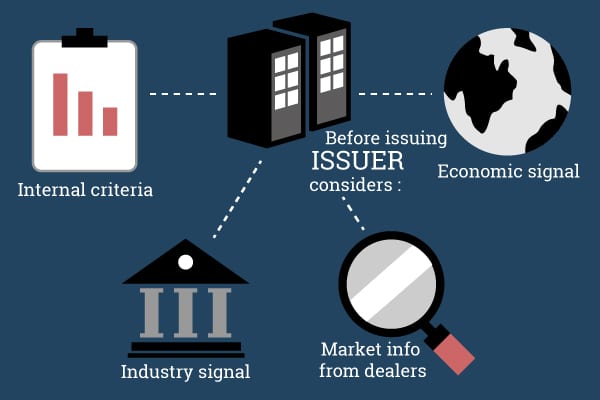

On one side, you have issuers who are looking to keep their cost of capital low, while also carefully managing risk—too high and the payout is not financially viable. A company looking to issue a sizeable bond—say, to finance a major acquisition, as Microsoft did when it bought LinkedIn in the summer of 2016 for $26.2B—will have a cadre of analysts and financial advisors monitoring the market to determine when it will be easiest, and cheapest, to issue debt.

Within a company looking to issue bonds, the treasury department’s major function is to maintain a healthy borrowing program, consisting of a strong investor base and an internal team who is well-informed about the capital market conditions. It is the job of the issuer to keep a watchful eye on the bond market in order to issue bonds while minimizing the cost and risks to achieve successful deal execution.

Also within an issuing company, the company CFO and treasurers take into account many economic signals, sector specific signals, their internal corporate finance criteria (such as debt to cash flow ratio, leverage, cash flow and credit ratings, just to name a few). These treasury teams also work with the debt capital markets (DCM) teams of several investment dealers, who provide professional services and client coverage. A big part of this coverage involves sending issuers information about pricing levels for new bond issues, timing to issue, and benchmarking with industry peers. Large corporations who issue bonds frequently typically also have an investor relations team to manage relationships with their major debt and equity investors.

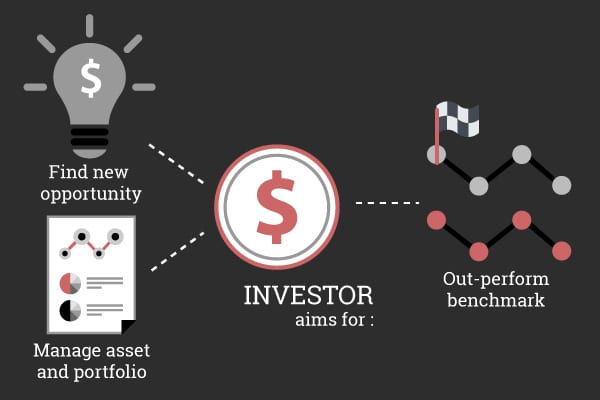

On the other side of this equation, you have investors, typically institutional funds such as mutual funds and exchange-traded funds (ETF), pension funds, life insurance companies and hedge funds. Institutional funds are pooled funds which can range anywhere from $10M to over $100B.

Large funds will typically have a portfolio manager who oversees all investment decisions, a credit analyst who analyzes investment opportunities, some of which is provided by dealers, and a trader who strategizes and executes the buying and selling of securities. In most cases, only institutional investors have access to primary bond sales through their investment dealer. Many large funds have direct relationships with issuers as well.

An investor’s main objective is to find new deal opportunities in which to invest their funds, in order to meet the performance objectives of their fund. In the bond market, they are often institutionalized, and are seeking to maximize profit for their portfolio. Fixed income investors manage their assets by either trading bonds in the secondary market or purchasing new bond issues directly in the primary market.

Connecting the Two Sides

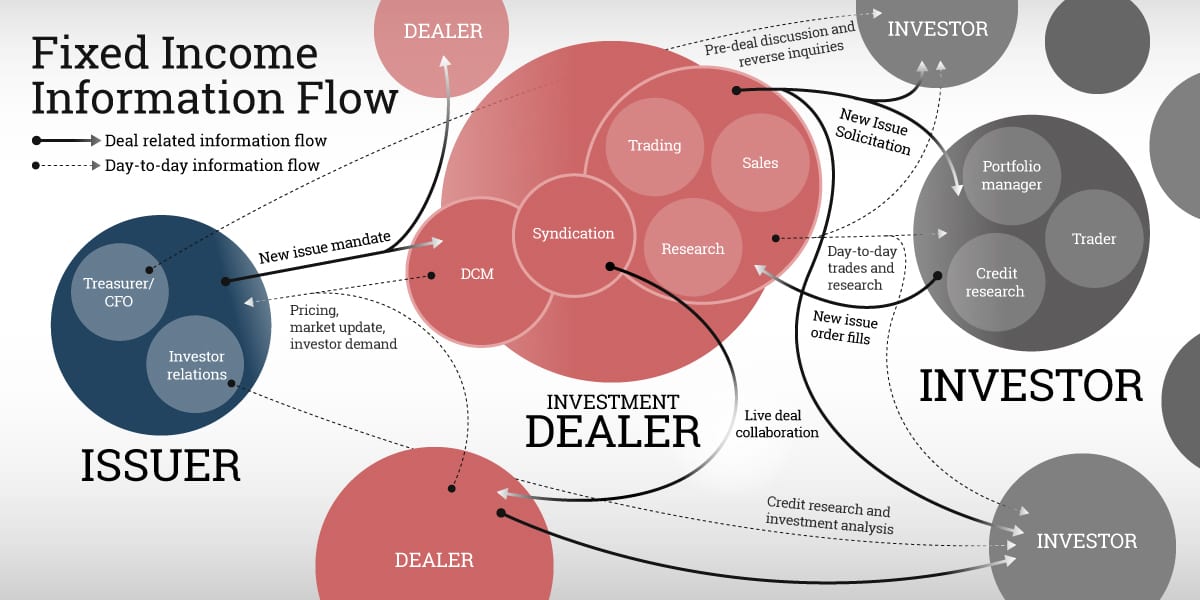

These two sides of the market require connectivity, however—this is where investment dealers factor into the market. The debt capital markets (DCM) teams are tasked with advising clients looking to raise capital on what type of debt will best meet their needs and on what terms. They are involved in every aspect of structuring and executing new debt issues – working with issuer clients to determine the right structure, working with legal counsels to document the deal, and working with internal teams including syndication, sales and trading desks to price and distribute it. Their main objective in the market is to connect issuers and investors, and to execute large and often complex transactions smoothly and efficiently.

They play the role of expectation manager, as well, through their role in communicating information between the two stakeholders in a fixed income deal. To do this, DCM teams maintain relationships with issuer clients by providing market research and data constantly so that they are in a position in order to execute new issue transactions successfully.

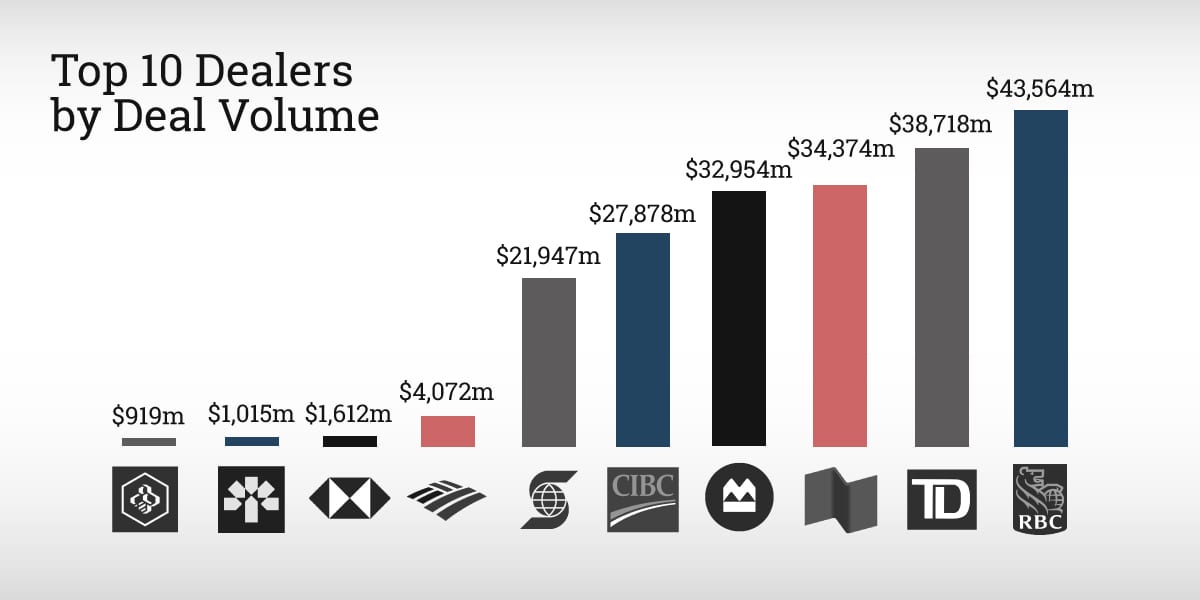

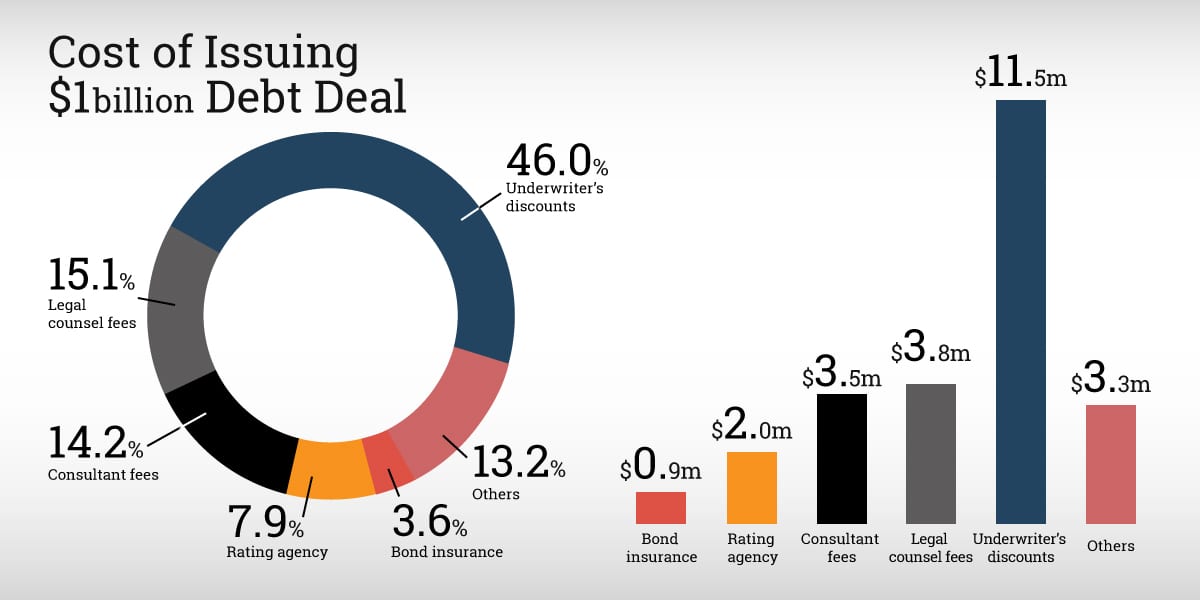

The major dealers in Canada are the big 6 banks, whose DCM teams are around 30 – 60 people. There is fierce competition between the banks to act as the bookrunner or lead for a new bond issue, and in order to maximize their commission they must ensure that best practices are followed. Typically bookrunner commissions range between 0.3% – 1.5% of the total deal (i.e. for a $1 billion deal, commission will range from $3M – $15M). Within an investment dealer, DCM teams work with the Syndication team, who provide a channel to Sales, Trading and Research departments.

The majority of new bond issues in Canada are syndicated, which allows dealers to spread risk and take part in financial opportunities that may be too large for their individual capital base. Investment dealers within a syndicate group will typically split the fee based on an issuer’s discretion.

Through dealers, issuers are able to finance large scale projects by accessing investors, but each lacks full insight into the motivations and incentives of the other.

Thomson Reuters, 2016

Illiquidity on the Rise

The problems that exist in the North American bond market today are mainly due to its decentralized structure of being primarily OTC (over-the-counter), fragmented data and asymmetric information flow. Due to relative bargaining power and access to information, larger investors and dealers develop an inherent competitive advantage in the marketplace.

A result of this fragmented and limited data environment has been a decrease in liquidity throughout the market. Since there is no central hub connecting the various players in the market, there is also limited information flow. This results in high search costs, which represent the opportunity cost of researching a product or service for purchase: without a complete picture of the information, investors and issuers are forced to piece together information from a variety of different sources and dealers in order to accurately generate the appropriate analysis for the deal.

In addition, many regulators have flagged the lack of access and non-transparent order allocation as a problem. Only the biggest institutional funds have access to new bond issues, and discrepancies in fill rates exist depending on timing, size, demand and relationships. As a result, on average only 5 to 20 per cent of an investor’s orders are filled.

The market, as it currently exists, is opaque rather than technology-based. It is manual and inefficient, and it has ultimately impeded the growth and functionality of the bond market.

Global capital markets are increasingly headed towards a crisis of liquidity. At the same time, electronic secondary trading is on the rise, demonstrating the increased efficiency that digitization and automation can bring to the market. At the confluence of these two trends lies an opportunity to, once and for all, bring global capital markets out of the twentieth century and into the twenty-first, and to modernize the way primary bond issuance is done.

This opportunity exists because of the current state of primary markets, and the many inefficient processes and characteristics that form the markets norms—norms that, while accepted, only serve to hold the market back amidst a time of immense change and innovation.

Information, for instance, is extremely decentralized. Information is fragmented, assembled in bits and pieces and disseminated only through manual exchanges between issuers, dealers, and investors. There is an obvious need for centralization of information—a single hub where information such as price discovery, information gathering, and negotiation can be done, so as to be transparent and efficient. Since there is no centralized hub, issuers and investors alike are forced, essentially, to paw around with only partial awareness of the opportunities around them; if they land on a good deal, that’s great—but how would they know if they missed one? Dealers can not fill this role adequately, either, since no one dealer has—or could ever have—all the information and resources required. For issuers and investors, this means: higher transactions costs, a more laborious transaction process, and time spent assembling the deal.

This is an opaque system that in many respects, fails to accomplish its primary goal—matching investors with issuers—efficiently and quickly. In an age when automation in financial markets offers a fundamental shift in the way the markets operate, why does the primary capital market need to be left in the past?

The answer is that it doesn’t.

Opportunities Through Tech Enablement

Digitization and automation is the key that will unlock a host of efficiencies, improvements, and in the end profits, for the primary bond markets. By allowing issuers and investors to complete the deal in an environment with a centralized repository of data and information, the element of uncertainty—is this the best deal? Am I getting the best terms?—is eliminated. Moreover, the laborious aspects of deal completion (like research, price discovery, and opportunity discovery) are all automated and reliant on powerful AI algorithms.

Increasing Transactional Efficiency Through Matchmaking

By shifting the process of issuer/investor matching towards a more digitized system based on proprietary algorithms and machine learning, investors can have investment options curated for them, matching their specific criteria, risk profile and pricing terms. Not only does this make things easier for the investor, but it also brings their costs down: in such a system, investors will save significantly on search costs and price discovery costs, freeing up time and resources to spend on more important aspects of closing the deal such as research and due diligence. These processes can take up to two weeks for credit analysts to fully research a new company.

By removing some of the more arduous aspects of this process, issuers stand to reduce 50 per cent of the transaction costs simply in efficiencies within the searching and price discovery stages. By freeing up time and resources previously dedicated to the processes related to a single deal, investors have the capacity to work on analyzing more investment opportunities. With powerful matching technology, investors will be presented with a range of investment opportunities, including many that may not have previously been on their radar. Sophisticated matching algorithms are already used in many dating websites and even by tech giant Amazon for their popular recommendations, which helps you choose items to buy based on millions of real-time data points. Using this technology to discover investment opportunities instead of traditional OTC conversations, investors will have access to more issuers, and vice versa.

Preventing ‘FOMO’ For Deals Through More Frequent, Opportunistic New Issues

Currently, investors rely on manual interactions with multiple dealers for most of their deal flow, who act as the middleman. Smaller investment firms, however, are at a disadvantage—dealers tend to service larger funds more than smaller ones due to the large order size of new debt issues. In addition, no single dealer has a complete picture of all activity in the primary markets. All investors, and especially asset managers at smaller funds, suffer from ‘FOMO’ (fear of missing out) of good deals due to blind spots. By levelling the playing field through the curation of investment ideas, all investors can be brought into the fold, which ultimately allows for more flexibility across the process of the deal. A firm who needs a smaller issuance won’t have to deal exclusively with investors who deal in larger amounts, and so on.

This would usher in significant change in the Canadian bond market. Currently 90 per cent of issuance volume in Canada is syndicated, in order to achieve liquidity and mitigate risk—a byproduct of the reality that issuers do not issue smaller bonds, and do not issue frequently. This is partially due to costs, which fintech solutions can help reduce. By bringing down the price discovery, research and transactional costs by as much as 50 per cent, there is less financial barrier to smaller, more frequent issuances.

Things like search costs, regulatory filings, clearing and settlement costs, draw costs and marketing road show costs can all be streamlined so that issuers can be more opportunistic to issuance based on market conditions and investor demand. In a simplified system, the costs that accumulate purely as a result of navigating a complicated network—including legal costs and time spent on manual tasks—fall by the wayside. The result is a deal that is more profitable and less expensive for both issuer and investor.

Haas Institute, UC Berkeley

Increasing Transparency, Efficiency, and Liquidity

The technology is only one part of the picture, of course: other improvements resulting from technological innovation are harder to categorize, but no less important. The result of this level of innovation is that it allows market participants to behave differently—they will be able to spend more time looking into the health of a company than on the terms of a particular deal; they will be able to access a far wider market than they do currently, and will be able to do so on the back of an increased foundation of trust that results from a fully transparent, centralized repository of historical market information for the entire fixed income marketplace.

Looking forward, the implementation of this technology is no less consequential than the introduction of digital trading in the stock markets, or multi-dealer access. By revolutionizing the entire way bonds are issued, through an end-to-end digitized, transparent process, technology leads to increased activity, engagement, and trust. Ultimately, this is the direction the industry is going; the outdated manual methods are not sustainable in an increasingly digital world. This sort of change has already come to equities markets—digitization has changed the game in those markets, and it has the potential to do the same for the bond market.