The following article is based on research by Marshall Gittler, Head of Investment Research for FXPRIMUS.

FXPRIMUS Week in Focus for the week beginning 23 Jan: preliminary PMIs, UK & US Q4 GDP, Australia, NZ and Japan CPIs

It’s a week without many major economic indicators and no central bank meetings. In their absence, the focus will be on politics.

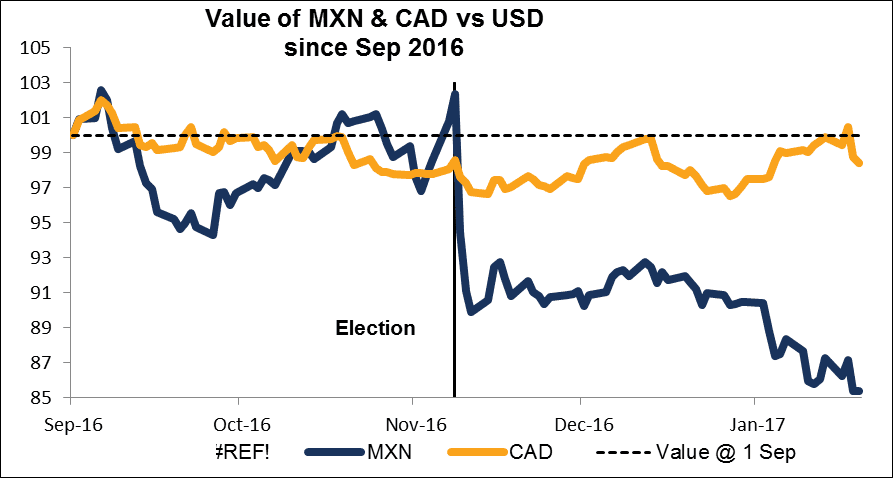

First, US politics. President Trump has promised to issue a slew of executive orders immediately upon taking office, not to mention possibly giving notice about wanting to renegotiate the North American Free Trade Agreement (NAFTA) with Canada and Mexico.

So far, MXN has been the barometer of Trump policy, given Mexico’s dependence on trade with the US. The currency has fallen a lot already, but just because something is down doesn’t mean it can’t go down further. Mexico has other problems of its own as well – for example, riots at the gasoline pumps recently. CAD could also be hit as it is also heavily dependent on trade with the US.

The other political point of interest this week will be Tuesday’s ruling by the UK Supreme Court on the Government’s Brexit plans. It’s quite likely that the Court will rule Parliament has to sign off on any Brexit plans, but the Government seems well prepared for this possibility. The surprise would be if the Court rules that the Government also needs to get the approval of the devolved authorities, such as the Scottish Parliament. GBP could gain significantly if the Court does so rule.

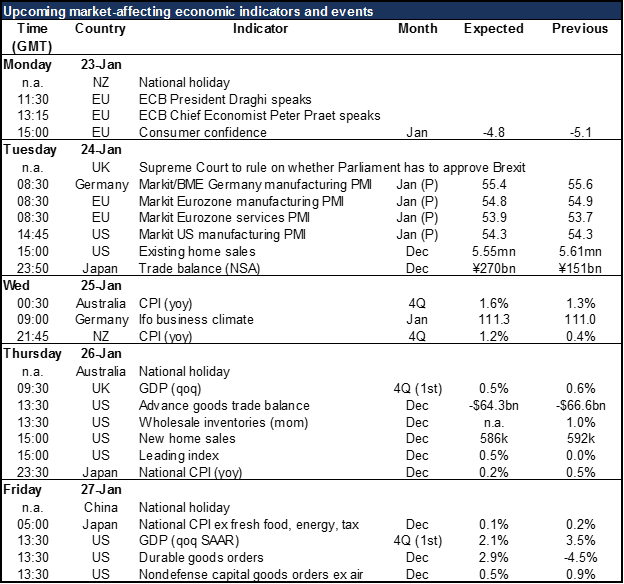

As for this week’s indicators, the focus will be the preliminary Markit PMIs for Europe and the US on Tuesday. Not much change is expected this month, so the market movement depends on what surprise if any we get from them.

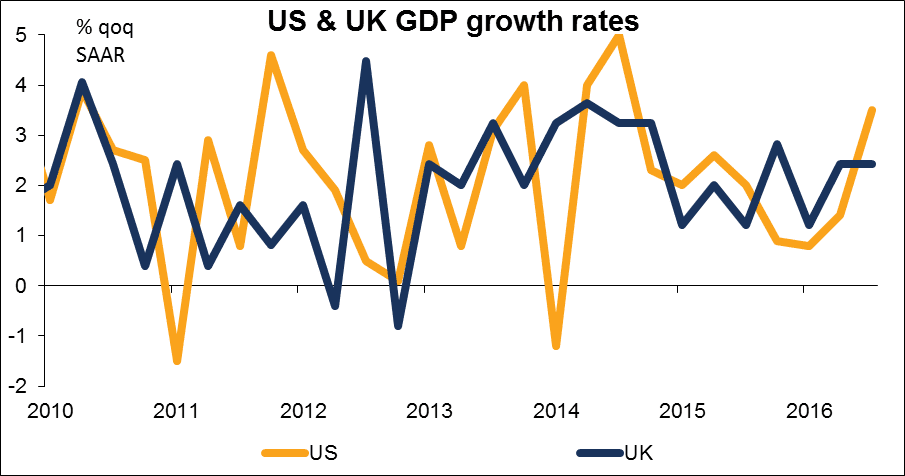

UK Q4 GDP is forecast to slow slightly, but nonetheless remain at a relatively robust level. That might support the pound. US Q4 GDP is expected to slow considerably however. A higher-than-expected result for the US would therefore be more of a surprise than a miss, so the USD could gain on that indicator if there’s a positive surprise.

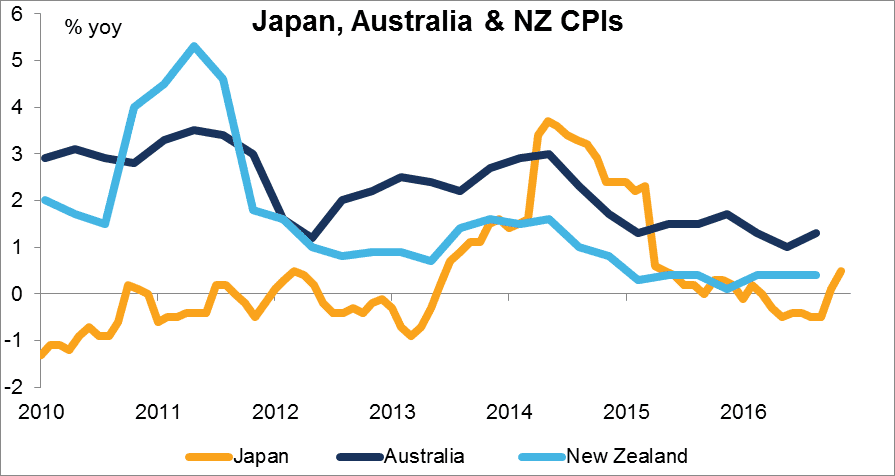

Elsewhere, we’ll get a firmer grasp on the world inflation picture this week as Australia, New Zealand, and Japan release their CPIs. Australia and New Zealand are both forecast to show a substantial rise in the yoy rate of price increases. That could increase the odds of a tightening and push their currencies – which have been the best-performing G10 currencies so far this year – still higher.

Japan remains the odd man out with regards to inflation as that nation’s inflation rate is expected to slow. That’s why I think the yield spread is likely to move further against the yen and encourage its use as a funding currency Furthermore, some 19% of its exports go to the US, so it too may be hit by President Trump’s new trade policy. I expect the yen to weaken.